The Indian market (Nifty Fut) slips Tuesday on

subdued global cues and the concern of RBI autonomy. The Indian market (Nifty

Fut/India-50) closed around 10775 Monday, surged by almost +0.83% on positive

Asian cues, lower USD, lower oil and hopes of RBI truce with the government

coupled with a survey that BJP will win almost 300 seats alone in the

forthcoming general election. The market was already discounted that the RBI

governor will not resign after his meeting with

the PM and FM last week.

So far Nifty rallied almost +3.63% in November

after a plunge of almost -11.40% in October and September on higher USD, higher

oil, negative global cues, NBFC/HFC liquidity crisis (default-ILF&S),

hawkish RBI and “war of words” between the RBI and the Indian government.

All eyes were on the RBI board meeting on Monday.

After almost 9-hours of marathon meeting, it seems that although there may be a

truce, for the time being, RBI blinks

first and as per the government directive and will increase liquidity (cash

flow) in the system. Some of the regulatory power of RBI/MPC will be shared by

government appointees BFS (Board for Financial Supervision) or simply by the

RBI board. This raises a serious question of central bank independence

(autonomy) and RBI/MPC may now function like a corporate board rather than an

independent institution, free of political interference.

The government basically wants the RBI to take an

“accommodative” stance in lieu of “calibrated tightening” in this global era of

dual QT and in the process has entered into an elite membership of some

countries, which are now actively interfering in central bank’s monetary policy

(Argentina, Turkey and the US/Trump). The Indian government is now “desperate”

to kick-start lending to the MSME sector

in a big way ahead of the election, which could cause a big surge in NPA/NPL in

the years ahead as a result of such political populism. The government is also

eyeing the RBI surplus to fund its fiscal deficit, a plan which may be unheard

before in the history of central banks.

Technical

Aspect:

Updated:

10:00

Nifty-SGX-NF:

10727 (-40; -0.37%)

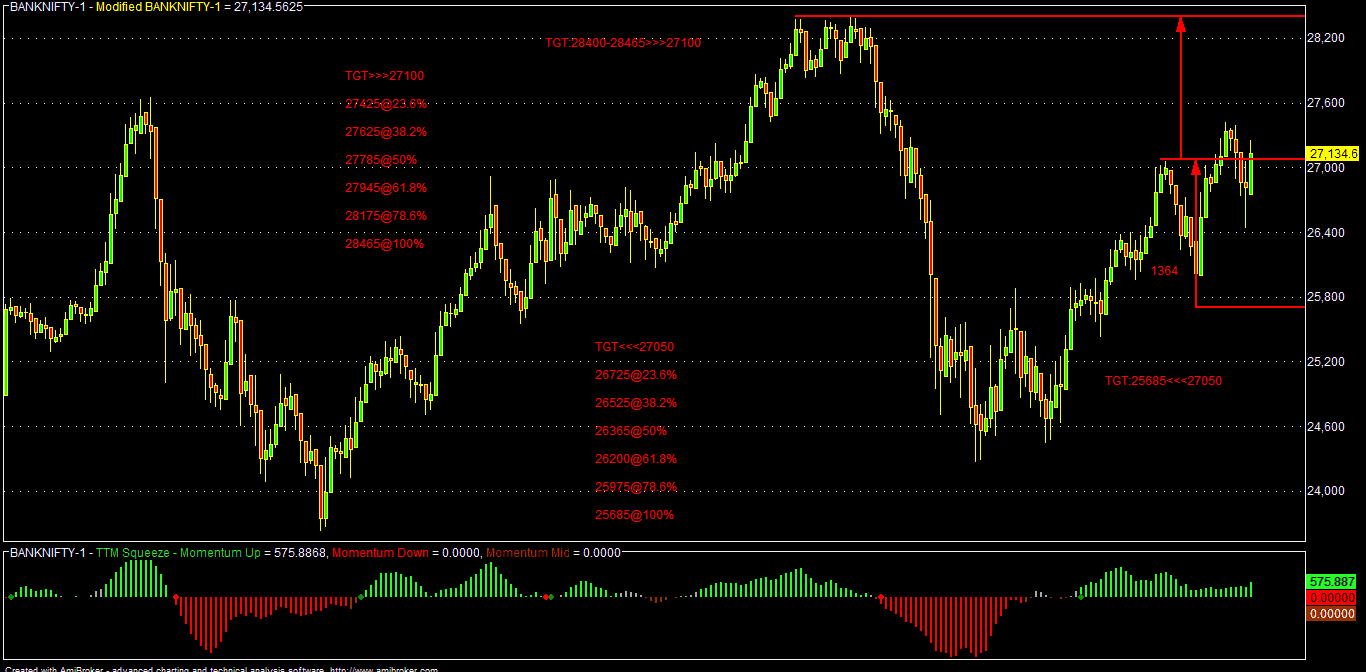

Bank

Nifty-BNF: 26220 (-99; -0.38%)

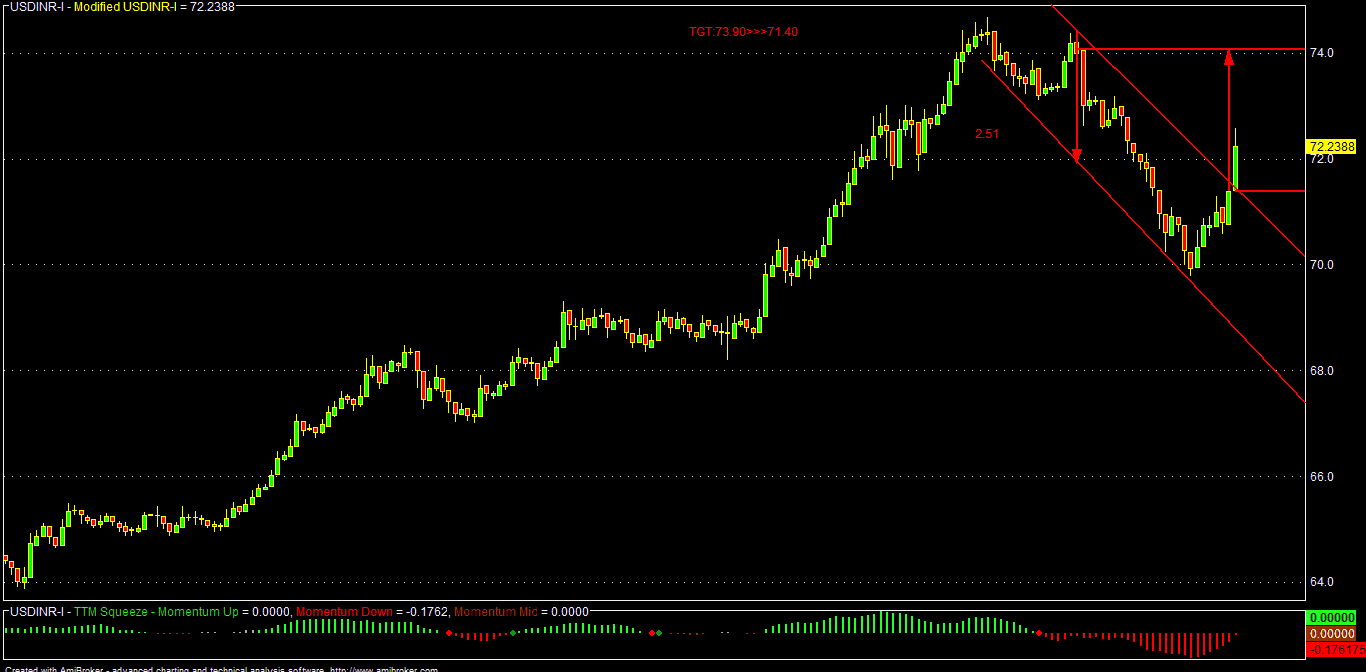

USDINR-I:

71.39 (-0.34; -0.24%)

SPX-500: 2688 (-8; -0.32%)

Fut-I (Key Technical Levels)

Support for NF:

10690/10635*-10595/10550-10495/10450-10410/10340-10300/10270

Resistance to NF:

10785/10805*-10875/10905-10975/11025-11085/11165-11230/11295

Near-term broad range: 10000-10805

Support for BNF:

26250/26050*-25900/25700-25425/25350-25200/24950-24850/24600

Resistance to BNF:

26400/26550*-26700/26900-27200/27350-27550/27750-28000/28200

Near-term broad range: 24250-26550

Support for USDINR-I:

71.65/71.20-70.90*/70.45-70.15/70.00-69.70/69.30-69.00/68.25

Resistance to USDINR-I:

72.10/72.55-72.85/73.35-73.75/74.05-74.35/74.75-75.00/75.65

Near-term broad range: 70.90-74.75

Support for SPX-500:

2680/2645*-2620/2590-2580/2560-2535/2520-2490/2445

Resistance to SPX-500:

2700/2725*-2755/2775-2795/2820-2835/2860-2880/2905

Near-term broad range: 2590-2820

Technical

View (Nifty, Bank Nifty, USDINR-I, SPX-500):

Technically, Nifty Fut-I (NF) has to sustain over 10805 for a

further rally to 10875/10905-10975/11025-11085/11165-11230/11295 in the near

term (under bullish case scenario).

On the flip side, sustaining below 10785-10765/10725 NF may fall to 10690/10635-10595/10550-10495/10450-10410/10340

in the near term (under bear case scenario).

Technically, Bank Nifty Fut-I (BNF) has to sustain over 26400

for a further rally to 26550/26700-26900/27200-27350/27550-27750/28000 in the

near term (under bullish case scenario).

On the flip side, sustaining below 25350-26250 BNF may fall to 26050/25900-25700/25425-25350/25200-24950/24850

in the near term (under bear case scenario).

Technically, USDINR-I has to sustain over 71.65 for a further

rally to 72.10/72.55-72.85/73.35-73.75/74.05-74.35/74.75 in the near term (under bullish case

scenario).

On the flip side, sustaining below 71.20, USDINR-I may fall to 70.90/70.45-70.15/70.00-69.70/69.30-69.00/68.25

in the near term (under bear case

scenario).

Technically, SPX-500 has to

sustain over 2725 for a further rally to 2755/2775-2795/2820-2835/2860-2880/2905

in the near term (under bullish case scenario).

On the flip side, sustaining below 2715-2700 SPX-500 may fall to 2680/2645-2620/2590-2580/2560-2535/2520

in the near term (under bear case

scenario).

Valuation metrics:

Nifty-50: 10700; Q2FY19 EPS: 413.70; Q2FY19 PE:

25.86; Avg FWD PE: 20; Proj FY-19 EPS: 425-450; Proj Fair Value: 8500-9000

Bank Nifty: 26200; Q2FY19 EPS: 495.50; Q2FY19 PE:

52.88; Avg FWD PE: 20; Proj FY-19 EPS: 961-1000; Proj Fair Value: 19220-20000

(assuming NPA recovery).

SPX-500: 2700; TTM Q2-2018 EPS: 123; TTM PE:

21.95; Proj 2019 EPS: 150-160; Avg FWD PE: 18; Proj 2019 EPS: 150-165; Proj

Fair Value: 2700-2970

NIFTY FUT

BANK NIFTY FUT

SPX-500

CRUDE OIL-WTI