Market

Wrap: 28/02/2017 (19:00)

Meanwhile

India’s Q3FY17 GDP flashed as 7% against consensus of 6.4% (QOQ: 7.3%; YOY:

7.2%) trashing all the DeMo blues by accounting only “available data currently”;

i.e. only formal part of the economy (??); As par CSO: “impact of policies like

DeMo difficult to assess with a lot of data”.

Will

market believe this “surprised” GDP data, which basically said that there is

actually no impact of DeMo on the economy even in Q3FY17?

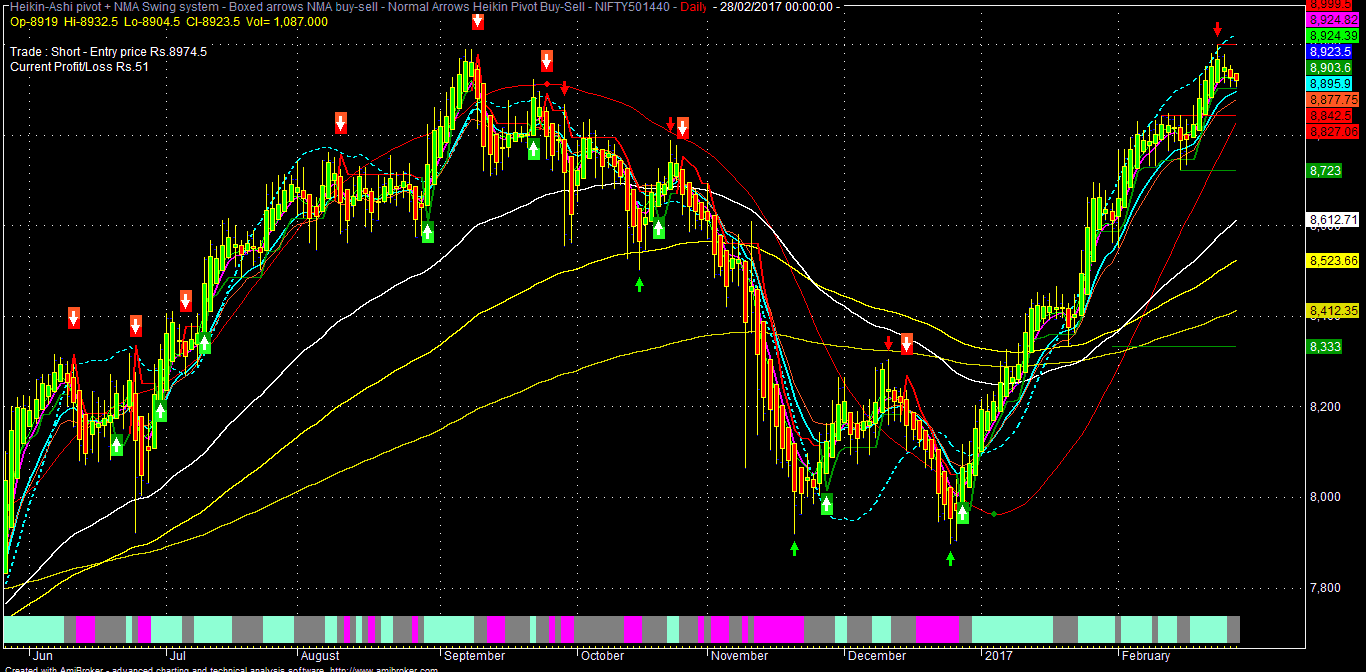

Looking at the chart, Nifty Fut (March @8913)

has to sustain over 8995 area for further rally towards 9035-9075 &

9125-9195 in the short term (under bullish case scenario).

On the other side, sustaining below 8975

zone, NF may fall towards 8910-8875* & 8815-8765 area in the near term

(under bear case scenario).

Similarly, BNF (LTP: 20695) has to

sustain over 20950 area for further rally towards 21050-21150 & 21350-21500

area in the near term (under bullish case scenario).

On the other side, sustaining below

20900-20750 area, BNF may fall towards 20600*-20500 & 20250-20000 zone in

the near term (under bear case scenario).

Nifty

Fut (March) today closed around 8913 (-2 points), almost flat after making an

opening session high of 8938.45 and day low of 8884.15. The Indian market today

opened almost flat on the back of mixed global cues ahead of Trump’s much

awaited congressional speech and confusion of any specific trajectory of his fiscal/infra

spending plan. But, soon after opening in slight positive zone, domestic market

fall into negative zone on the concern of a tepid Q3FY17 GDP as a result of

DeMo.

The

market sentiment improved somewhat, after OECD predicted India’s FY-17 GDP

growth as 7% and 7.3% & 7.7% for FY: 18 & 19. Also, India’s Economic

Affairs Secretary (Das) reaffirmed in the same OECD venue that states are ready

to implement GST from July’17 and as such there should not be any issue to roll

out of the same by then. All these positive commentary made the NF to respect

the 10-dema, currently around 8890 and the market saw some short covering/value

buying, especially in some of the GST related stocks and closed the day almost

flat.

Indian

market today was dragged by BPCL (after ONGC-HPCL deal, which may be negative

for the sector, at least in the short term because of high leverage concern),

Grasim (for capex concern after Idea-Vodafone deal?), private banks &

financials, auto (concern of poor Feb sales nos) and FMCG stocks.

Nifty

was well supported today by sudden spurt of Bhel in the last hour of trading

session apart from Bharti Airtel, Yes Bank, Asian Paints.

After

market hours today, India’s fiscal deficit (Apr-Jan) flashed as Rs.5.64 tln,

which is almost 105.7% of FY-17 target. Infrastructure/core sector output came

as 3.4% against 5.7% (YOY). But most surprisingly Q3FY17 GDP growth was stated

as 7% against consensus of 6.4% (QOQ: 7.3%; YOY: 7.2%), defying all the DeMo

blues.

Q3FY17

GVA flashed as 6.6% against estimate of 6.1% (QOQ: 7.1%; YOY: 6.9%). CSO also

projected FY-17 GDP growth as 7.1% against estimate of 6.4% YOY: 7.9%).

Overall,

apart from construction & financial sector, almost all the other sectors

showed remarkable resilience in Q3, even in the back drops of the DeMo. Even

private consumption expenditure was grown by 10% against 7.5% sequentially.

Also gross fixed capital formation was up by 3.5% against decline of 5.6% on

QOQ basis. But the most significant contribution of the Q3 GDP may be the Govt

consumption expenditure, which was up by 19.9% against 15.2% sequentially.

As

par CSO, improvement in GVA and stable GDP in Q3FY17 is because of increase in

taxes & fall in subsidies; but gross capital formation is a matter of

concern, which falls below 30% in FY-17. CSO also maintained that GDP numbers

announced today by taking only available data currently and it’s very difficult

to assess impact of DeMo so quickly, as it involved lots of data.

Thus,

basically today’s 7% GDP data may be taken into account only the available data

from the formal (organized) sector of the economy and may not reflect the

severe economic disruption by the informal (unorganized) sector of the economy

as a result of DeMo. We may know more about the true figure of Q3 GDP only by

May’17, when CSO will release the final estimate, taking into more available

data. Thus, final GDP number may vary significantly after taking into account

full impact of DeMo (??).

There

were visible slides in various economic activities and sudden dips in PMI data

after DeMo; but despite that it seems that CSO did not take into account all of

the DeMo data including surge in bank deposits and in that scenario, market may

look into the PMI and other high frequency data in the coming days to assess

the actual impact.

In

the days ahead, we may know more about the Q3 GDP number released today as

experts will certainly analyze it more minutely. But, a sudden dip in CPI in Q3

may also be one of the reasons for today’s surprised number (GDP output in

current prices – inflation?). Also, as par EX-CSO, difference between Q3 GVA

& GDP (6.6-7%) may be due to pre-payment of taxes and GFCF is based mainly

on consumption of steel & cement, which is a byproduct of incremental Govt

infra spending.

In

any way, when an economy is growing at a projected rate of 7.5-8% year after year,

it does not need any incremental rate cuts from RBI also. If there is no Trump disappointment

today, Nifty may open gap up tomorrow on the back of better than expected GDP;

but the key question may be that will the market really believe it or not?

Watch 8995-9015 area in NF for any

breakout; otherwise it may be again sell on rise.

SGX-NF

BNF