Market Wrap: 17/04/2018

NSE-NF (April):10549 (+6; +0.06%)

NSE-BNF (April):25533 (+3; +0.01%)

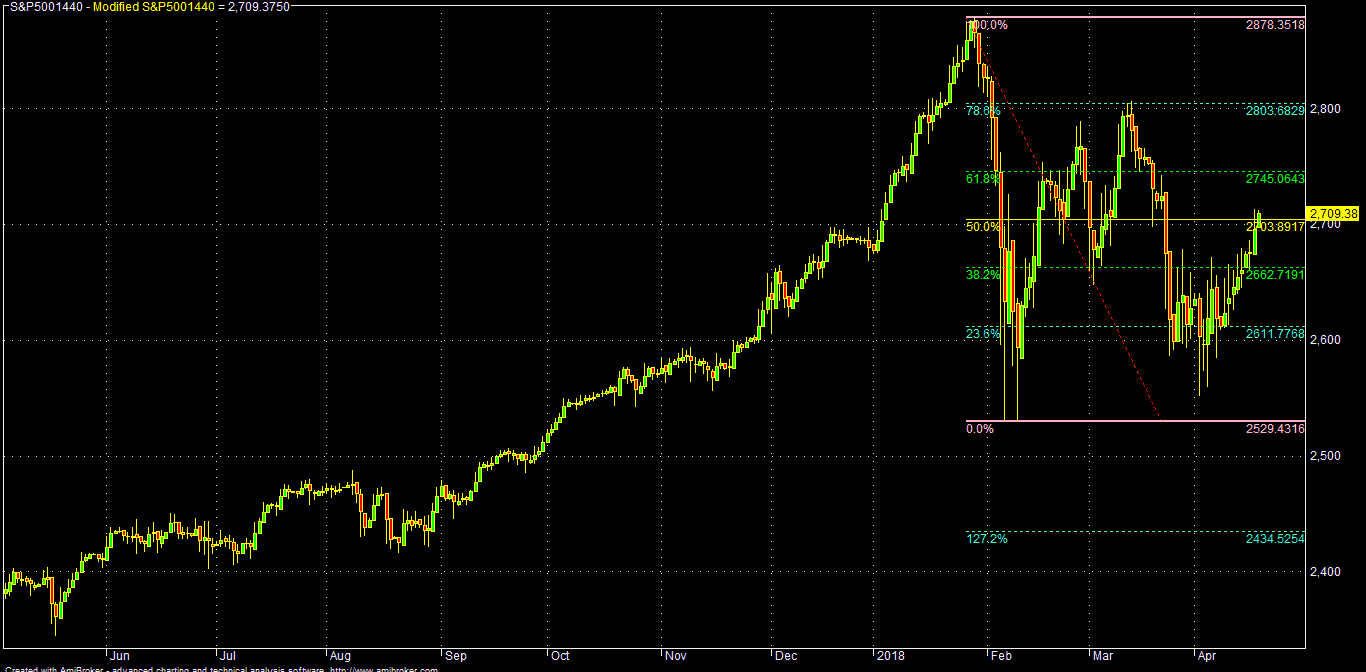

SPX-500: 2706 (+29; +1.07%)

Market Mantra: 18/04/2018

Updated: 08:00

SGX-NF: 10595 (+46; +0.44%)

Expected BNF opening: 25445 (+0.45%)

SPX-500: 2710 (+3; +0.13%)

(Gap-up opening on positive global/US cues amid surge in Netflix and other tech shares on upbeat earnings; but banks and financials were under pressure on muted report card; report of direct telephonic talks between US President Trump and North Korean President Kim has also boosted the risk-on sentiment; but surge in Hong-Kong-HIBOR rate have also affected the regional market sentiment).

March-Fut (Key Technical Levels)

Support for NF:

10570/10520-10480/10430-10400*/10370-10340/10280

Resistance to NF:

10615/10655-10675*/10725-10765/10815-10865/10915

Support for BNF:

25200/25050-24950*/24800-24600/24400-24250/23950

Resistance to BNF:

25450*/25655-25775/25850-26050/26150-26300/26525

Support for SPX-500:

2690/2675-2655/2640-2610/2595

Resistance to SPX-500:

2720/2730-2750/2765-2785/2805

Technical View (Positional-Nifty, Bank Nifty, SPX-500):

Technically, Nifty Fut-I (NF) has to sustain over 10615 for a further rally towards 10655/10675-10725/10765-10815/10865 in the short term (under bullish case scenario).

On the flip side, sustaining below 10595-10570 NF may fall towards 10520/10480-10430/10400-10370/10340 in the short term (under bear case scenario).

Technically, Bank Nifty-Fut (BNF) has to sustain over 25500 for a further rally towards 25655/25775-25850/26050-26150/26300 in the near term (under bullish case scenario).

On the flip side, sustaining below 25450, BNF may fall towards 25200/25050-24950/24800-24600/24400 in the near term (under bear case scenario).

Technically, SPX-500 now has to sustain over 2730 for a further rally towards 2750/2765-2785/2805 in the near term (under bullish case scenario).

On the flip side, sustaining below 2720, SPX-500 may fall towards 2690/2675-2655/2640-2610/2595 in the near term (under bear case scenario).

Valuation metrics:

Nifty-50: 10549; Q2FY18 EPS: 410; Q2FY18 PE: 25.73; Avg FWD PE: 20; Proj FY-18 EPS: 418; Proj Fair Value: 8360

Bank Nifty: 25334; Q3FY18 EPS: 820; Q2FY18 PE: 30.90; Avg FWD PE: 20; Proj FY-18 EPS: 961; Proj Fair Value: 19220

The Indian and global market story on 17/04/2018:

The Indian market (Nifty Fut/India-50) closed around 10549 on Tuesday, edged up by almost 0.06% on positive global cues, surprised China RRR cut @1% for some selected banks. The Indian market sentiment was also boosted by optimism about Q4 earnings and normal monsoon forecast by IMD this year and hopes of a speedy NPA resolution under NCLT/IBC mechanism.

The market sentiment was also buoyed by another report that RBI may extend NCLT resolution time frame for another 180 days and may also dial back partially its February circular banning all the existing CDR (corporate debt restructuring) routes so that banks will not require making provisions for the same in Q4FY18. Nifty Fut-I made an opening minute high of around 10568 and mid-day low of 10501 before closing around 10549 amid positive EU cues in a day of moderate volatility.

Indian 10Y bond yield edged up to 7.527% from 7.489% earlier and well off the RBI induced low of 7.123% as oil is surging higher, which may make fiscal discipline task of the government tougher. As a reminder, a higher bond yield is bad for the banks in addition to corporate India. Almost 50% of the operating incomes for the banks, especially the public sector ones are dependent on their bond portfolio.

The recent shortage of cash at various ATMs across the country may be also affecting the market sentiment as it reminds the days of the DeMo last year. Although the government is assuring and downplaying the same, the reasons behind the sudden surge in cash requirement may be a harvesting season as well as marriage season in North India and over & above all, the forthcoming state elections.

But it also shows that India is still an informal cash economy to a large extent despite government effort of the digital and formal economy. Thus, acute shortage of cash at the ground level may again disrupt the informal economy and also the GDP of the country in the coming days.

On Tuesday, the market was also boosted by the 1st resolution of the NCLT/NPA cases (so-called “dirty dozen”), when VEDL’s bidding proposal for stressed Electrosteel was accepted by the NCLT. Resolution of several other stressed companies may be on the card in the days ahead as the 180 days RBI deadline is looming and this may be a great relief for the banks.

But the problem is that the acquiring companies in most of the cases are itself stressed and high balance sheets debt level like VEDL, JSW Steel or Tata Steel. These companies will most probably take additional debt from the same consortium of banks to fund the acquisition of the NCLT companies and thus it may be a simple transfer of bank debt to larger companies having huge credibility and much better managerial capabilities.

Looking ahead the success of the NCLT resolutions may depend upon the actual viability of the stressed project. The market is also concerned about the growing instances of corporate loan frauds after the PNB “loot” (theft) came into the limelight. It’s now clear that a significant part of the NPA (debt pile) may be unrecoverable as that is related to the corporate frauds having little assets left over for the recovery.

Apart from earnings, macroeconomy, global cues, the Indian market may also focus on the domestic politics and elections in the coming months in preparation for the 2019 general election, which may be also advanced by few months for the “one nation, one vote” concept.

On Tuesday, Nifty was helped by ITC, HDFC, ICICI Bank, RIL, HUL, Power Grid, HDFC Bank, Indian Oil, NTPC, M&M and others by almost 57 points (47+10), while it was dragged by Axis Bank, Infy, L&T, TCS, Kotak Bank, Maruti, Sun Pharma, Wipro, Bharti Infratel, Tata Motors, IBULLS Housing and others by around 34 point (24+10).

Overall on Tuesday, Indian market was helped by mixed private banks and financials, FMCG, metals, reality, consumption, energy, infra and MNC, while it was dragged by automobiles, techs, media, pharma, and PSU banks.

Global cues were positive during Indian market hours on Tuesday:

US stock future (SPX-500) was up by 0.47% at a 3-week high on expectations of strong S&P-500 Q1 corporate earnings results. Netflix was up by over 7% in pre-market trading after it reported better-than-expected Q1 earnings and guidance.

European stocks were up by 0.63% as automakers gained when China removed a two-decade restriction and will let foreign car makers own more than 50% of local ventures, which should boost foreign automakers profits. Also, exporters gained after EUR fell back from a 2-week high and moved lower, which is positive for earnings for European exporters. But, gains were limited in European stocks after subdued German-ZEW survey expectations of economic growth for April, highlighting the ongoing trade tensions instigated by Trump and a stronger EUR.

Overall, risk-on trade was encouraged by the limited fallout from a US-led strike on Syria over the weekend as a one-off, except for the occasional daily Israeli airstrike on Syria. The market sentiment was also improved on the US government's announcement it has not decided on additional sanctions on Russia, suggesting tensions between Moscow and DC are easing. The market was also buoyed as Trump dials back both the FX manipulation tweets and a threat of Russian sanctions.

Asian stocks closed mixed: Japan +0.06%, Hong Kong -0.83%, China -1.41%, Taiwan -1.32%, Australia unchanged, Singapore +0.03%, South Korea -0.17%, India +0.26% (Sensex).

China's Shanghai Composite fell to a 2-1/4 month low after China Mar industrial production rose +6.0% y/y, the slowest pace of increase in 7 months, and as technology stocks tumbled after the US banned ZTE Corp, China's second-largest telecommunications gear-maker, from buying American technology. Chinese bank stocks may get a boost in Wednesday's session as the PBOC, after Chinese markets closed Tuesday, cut some banks' reserve requirement ratio by 1.0%, effective Apr 25.

China’s GDP and other economic data were mixed on Tuesday:

China’s Q1 GDP print just met estimates (on a Y/Y basis and missed Q/Q) while industrial production in March came in below forecasts, but retail sales were upbeat: China Q1 GDP Y/Y meet at 6.8%, versus +6.8% exp. and +6.8% prior, China Retail Sales Y/Y beat at 10.1%, versus +9.7% exp. and +9.4% prior, China Industrial Production Y/Y miss at 6.0%, versus +6.3% exp. and +6.2% prior, China Fixed Asset Investment Y/Y MISS at 7.5%, versus +7.7% exp. and +7.9% prior.

Asia equity markets traded with a somewhat indecisive tone after the positive momentum from Wall St waned as the region digested mixed data releases from China including GDP. ASX-200 saw mild gains amid a slew of corporate updates, while Nikkei-225 was flat with price action contained by a firm JPY. Hang Seng and Shanghai were choppy in reaction to the mixed economic data.

European equities had shown strength on the back of improved risk sentiment with Syrian tensions continuing to abate. This is most noted in the materials and IT sectors, with both leading their peers. Negativity is noted in consumer discretionary, led by Reckitt on an analyst downgrade.

SGX-NF

BNF

SPX-500

GBPUSD

No comments:

Post a Comment