R-Infra has to sustain above multiple resistance zone

of 500-525 for 600-650;

Otherwise, sustaining below 480-460,

it may again come down to 440-414-370

For, R-Infra/ADAG : 2015 may be the year of deleverage---

A reflection Of Corporate India's increasing effort for the same in the coming days--

CMP: 493

Sell below 500 or on rise around 510-520-530

TGT: 480-460*-440-414-370 (1-3M)

TSL>535-545

Note: Consecutive closing above 525-545, R-Infra can further rally up to 555-575-600-650 in the near term in the alternative technical scenario.

As we all know, R-Infra is in great deleveraging mode for the last few months to prune its massive consolidated current BS debt of around Rs.26630 cr. The current standalone debt of R-Infra is around Rs.16500 cr with D/E ratio around 0.97 which is at par industry standard.

As par the management, the aim to make R-Infra debt free by FY-17 by selling various core (?) & non-core assets (BOT road projects, cement divisions, Mumbai Electricity Business). As par market reports, by selling these assets, R-Infra can raise up to Rs.30000 cr and as we all know, the company is entering big into defence business and basically changing its business profile. At the same time, R-Infra will concentrate more on its existing EPC business (smart cities, entire power chain, roads & metros). Thus, in future, EPC & Defence manufacturing sector will be the main focus area of the company.

R-Infra has already signed a non-binding agreement with PSP Investment of Canada to sell its 49% stake in Mumbai Power Transmission Business and as par reports, Cement business sale deal is almost final and will be officially announced by next week. Potential buyers are Blackstone, Carlyte, KKR and Ultratech. The Cement deal may be in the range of Rs.5000-6000 cr and the company is expected to get 50% of this amount after paring the relevant debt.

As par management, R-Infra has a portfolio of eleven BOT road projects (4600 km lane) at high growth traffic urban corridors (GQ & EW) at Delhi, Bangalore, Pune, Jaipur etc, in which it has invested around Rs.9000 cr and the company is confident to sell these road projects at a premium valuation of around Rs.11000 cr because of its premium locations and future revenue prospect.

Thus the company is expecting a gross amount of more than Rs.15000 cr from its road & cement assets sale and it is confident to be debt free (at least on standalone basis) by FY-17.

After selling these core & non-core assets (Road/Cement/Mumbai Power), R-Infra is expected to be debt free and will enter big into Indian Defence sector. As par the management, the Defence sector has relatively lower capital intensive and low gestation period with minimal regulatory uncertainties and have better ROE unlike road projects.

The likely size of the Indian Defence opportunities will be around $250 bln over the next ten years and the Govt is aiming to bring the defence import to around 30% by then on the back of NAMO's "Make In India" & "Skill India" initiatives. So it translates a domestic defence market of around $175 bln and R-Infra is expecting to get a sizeable chunk of that.

R-Infra has also hired experienced professionals from Defence industry at leadership position to foray into its Defence business initiatives. But there will be also severe domestic competition, which may come from M&M, Bharat Forge, L&T, RIL, Tata & Adani groups.

Few weeks ago, R-Infra has acquired around 35% stake for Rs.1669 cr with full management control in Pipavav Defence (active in Defence Ship building), which will be renamed as Reliance Defence & Engg Ltd. R-Infra has applied for various licenses and nods for wide range of Defence procurement in land & naval systems (like aircraft, helicopters, all-terrain combat vehicles, unmanned aerial vehicles, night vision devices, sensors, navigation and surveillance equipment, propulsion systems and simulators). R-Infra may invest another Rs.1200-1600 cr in Pipavav for the defence sector in the near term.

Another thrust area of R-Infra will be railways modernization & EPC, specially for metro rail and freight corridors. Currently, the EPC order book stood around Rs.4000 cr.

Few days ago, R-Infra entered into an agreement with a Russian Co (USC) for manufacturing four frigates for the Indian Navy, which is estimated for Rs.30000 cr spanning over next ten years. This shipbuilding exercise will be done at Pipavav's shipyard facillity.

In the just concluded Moscow visit, as a part of business delegation along with our PM, R-Infra Chairman signed an agreement with a Russian Co (Almaz Antey) to manufacture missile & radar system in India along with R&D and maintenance & overhauling for the Almaz systems already used by the Indian military.

Also there are some favourable policy announced on Pre-Christmas day regarding promotion of defence manufacturing in India under "Make In India" initiative and all the stocks associated with defence sector, including R-Infra has a good Santa Rally.

Now, all the above positive news flows regarding R-Infra is already known to the market and almost priced in by the scrip, which rallied by over 77% since late Sep'15 and more recently by over 33% since early Nov'15.

Looking ahead, ambitious foray & success into defence sector of R-Infra will hinge upon Govt's actual fiscal position and expenditure towards modernization of Indian Defence as huge amount is involved here and there are also many liabilities like 7-th Pay Comm including that of Indian Railways, OROP, pending bills of fertilizer & food subsidy etc, totaling around Rs.245000 cr. In that sens, it may be also tough for our Govt to keep the targeted fiscal deficit at 3.5% of nominal GDP by FY-17.

Also over reliance on Govt's "Smart City" theme may be counterproductive for R-Infra as there projects are still in the "visionary" state. If there is not so much "economic recovery" as expected in FY-17, Govt's fiscal position may not improve substantially and projected public expenditure by the Govt may also be in jeopardy.

In India, BOT road projects and also metro railway services are highly sensitive to political compulsions & popularism. Its not easy for operators to increase toll or fare incrementally higher to match with increasing input costs. Recent Mumbai Metro fare issue is such an example.

Some analysts are also skeptical about much hyped foray of R-Infra into defence sector without any clarity about the business model and related cash-flow. As of now, its too early to attribute any SOTP valuation to this defence business and one needs to wait, till the business is revenue (EPS) accretive.

The management of R-Infra has also indicated that the defence business will be negative on working capital (cash-flow) initially, but has an asset-turnover potential of around for times in future.

Some analysts are also believe that R-Infra's focus on defence & EPC business and together with steady cash-flow from the power distribution business (even after 49% proposed stake sale in Mumbai electricity) can create value for share holders in the long term with limited capex expenditure.

But ultimately with some revenue generating assets sales (both core & non-core) to prune massive debt, it will be interesting to see, how R-Infra's bottom line (EPS) will look like in the coming years.

Technically, the R-Infra scrip has strong strong zones around 500-525 and it has to close consecutively above this zone for next upside target of around 600-650 or even 700-735 in the mid to long term (FY:17-18).

For the time being, it has positional support of around 480-460 and sustain below that it may fall towards 414-370 area, where accumulation for portfolio investment may be good considering the favourable risk reward ratio.

As par BG metrics & current market parameters:

(on consolidated TTM & FWD EPS)

Present median valuation of R-Infra may be around: 550 (FY:15-16/TTM)

Projected fair valuations might be around: 590-635 (FY:17-18/FWD)*

* without considering the proposed assets sales & defence foray.

| SCRIP |

EPS(TTM) |

BV(Act) |

P/E(AVG) |

Low |

High |

Median |

200-DEMA |

10-DEMA |

| RELINFRA |

67.06 |

995.15 |

10 |

530.56 |

549.45 |

540.00 |

419.76 |

450.19 |

| RELINFRA |

70.95 |

1092.55 |

10 |

545.73 |

565.16 |

555.45 |

419.76 |

450.19 |

| RELINFRA |

79.75 |

1162.95 |

10 |

578.58 |

599.19 |

588.89 |

419.76 |

450.19 |

| RELINFRA |

92.5 |

1244.25 |

10 |

623.12 |

645.31 |

634.22 |

419.76 |

450.19 |

462.75 |

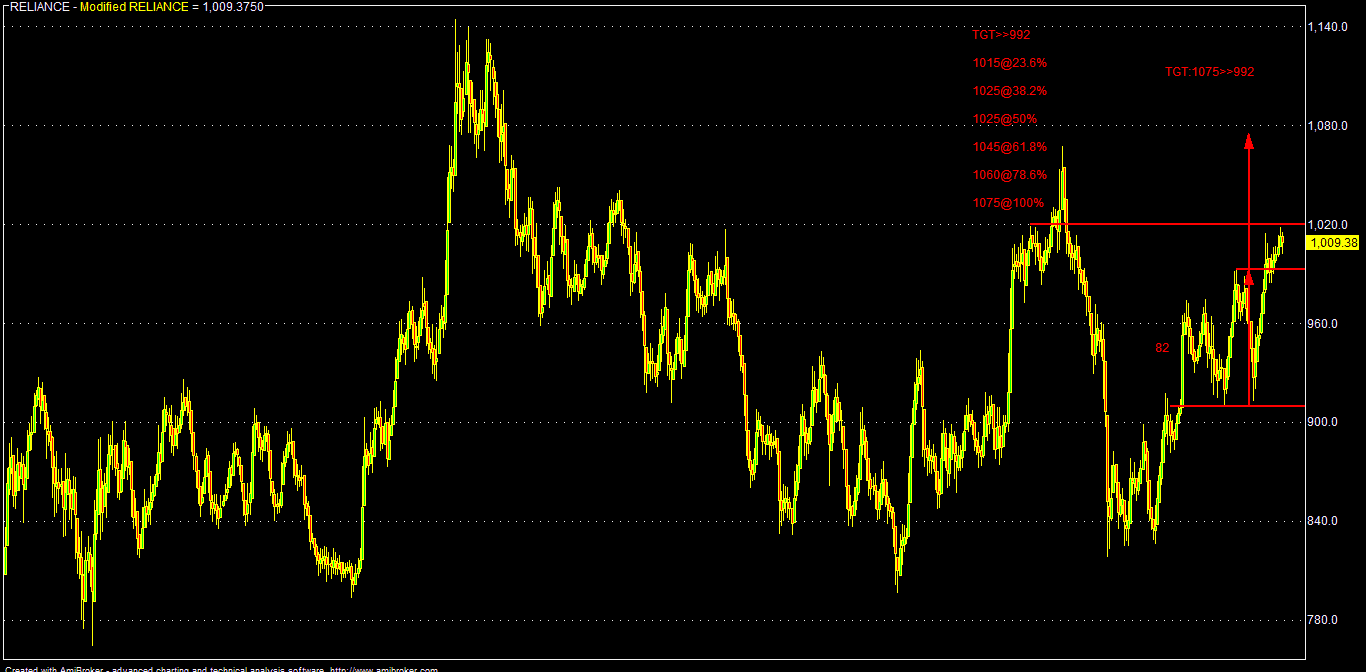

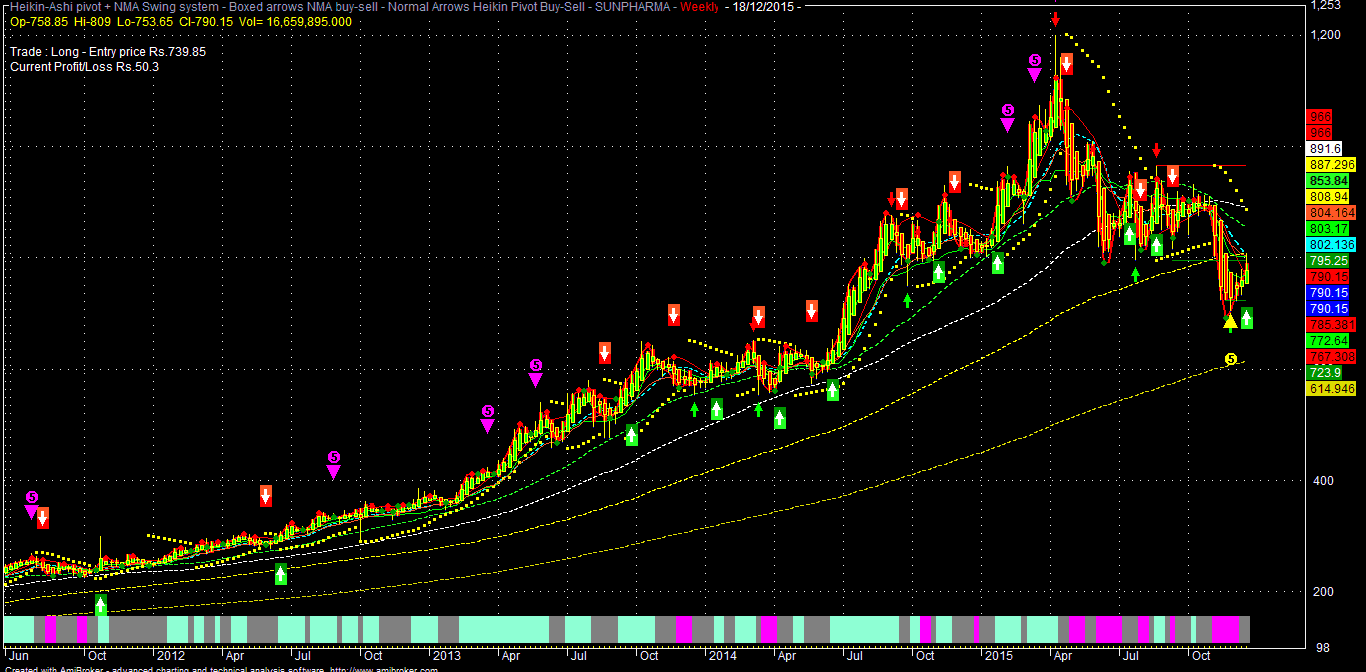

Analytical Charts:

.