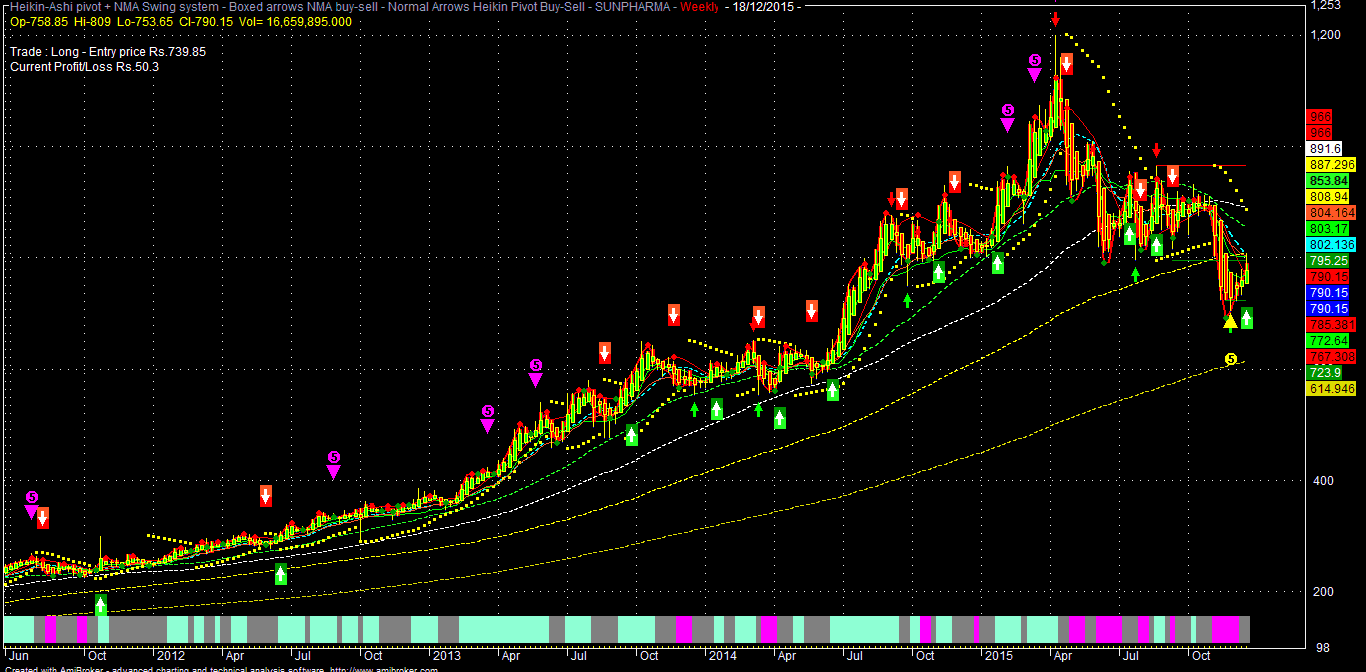

Sun Pharma has to sustain over 810-830 for any further upside;

Otherwise, it may again fall towards 720-700 zone.

Although the US FDA warning letter possibility regarding Halol Plant

was widely anticipated, it may not be fully discounted by the market yet.

CMP: 790

Sell on rise around: 810-830

TGT: 755-721-702-690*-675-655 (1-3M)

TSL> 850

Note: Consecutive closing above 850 for any reason, Sun Pharma may rally up to 875-895-916-966 in the near term in alternative bullish case scenario.

For Sun Pharma, it seems that "ghost" of Halol Plant (Ranbaxy) is still there. On last Friday, after market hours, the company disclosed that they had received the warning letter (WL) from US FDA on 18/12/2015.

Although this WL was widely expected after DRL fiasco, the same may not be fully discounted by the market yet.

Although the company is confident to resolve the issue, in the worst case scenario, an import alert may also be issued by US FDA in future for this Halol Plant, but the possibility of the same is lower, considering the integrity & professionalism of Sun Pharma management.

The company needs to disclose fully the contents of this warning letter publicly, but that may not be possible at this moment, unless US FDA disclosed that officially. The company is focusing on US FDA compliance for this Halol Plant, rather than transferring its manufacturing facillity to other compliant plants and is also taking necessary corrective measures for its other plants..

Analysts are optimistic that present WL is procedural in nature ( consistent with previous Form-483) and not something new, like data integrity etc.There is also no issue of global audit for all facilities from 3-rd party consultants (like DRL) and in that sense, the present WL issue may be the last negative thing for Sun Pharma in this issue. (Although the company is taking help of external consultants to ensure that its present remediation effort in plant automation and personnel training are completed in a time bound manner).

Thus there is low probability of any import alert in future from this Halol Plant. But there may be delay in new product approval from this Halol Plant as the company expects twelve months to resolve this issue with US FDA. The management believes that the present WL issue is for inadequate communication rather than any material remediation.

Analysts are cutting FY-17 EPS by around 6-15% and have new 12M TP, ranging between 762-950 (median TP 835) !!

This Halol plant contributes around 8% & 15% of Sun Pharma's global and US sales. Overall, more than 50% of the annual revenue comes from the US market for Sun Pharma. Incidentally, its the only plant in India from where Sun applied for product approvals for injectable drugs (apart from one such facillity in US). Thus, its also an important plant for Sun. Any clampdown (import alert) for this plant may take further 12-24 months to restore compliance standards (another Sun plant in Karkhadi, which received a US FDA import alert in 2014, is still yet to become US FDA compliant). Sun is already facing such US import bans for five of its manufacturing facilities in India.

As the present corrective steps are being implemented by Sun Pharma for the last one year, a WL means that additional effort is also required by the management for quick remediation of the same in the next twelve months. Till re-inspection is completed by US FDA, no new approvals is possible from this Halol Plant and the timing of the full resolution is quite uncertain as of now.

Analysts are optimistic that present WL is procedural in nature ( consistent with previous Form-483) and not something new, like data integrity etc.There is also no issue of global audit for all facilities from 3-rd party consultants (like DRL) and in that sense, the present WL issue may be the last negative thing for Sun Pharma in this issue. (Although the company is taking help of external consultants to ensure that its present remediation effort in plant automation and personnel training are completed in a time bound manner).

Thus there is low probability of any import alert in future from this Halol Plant. But there may be delay in new product approval from this Halol Plant as the company expects twelve months to resolve this issue with US FDA. The management believes that the present WL issue is for inadequate communication rather than any material remediation.

Analysts are cutting FY-17 EPS by around 6-15% and have new 12M TP, ranging between 762-950 (median TP 835) !!

This Halol plant contributes around 8% & 15% of Sun Pharma's global and US sales. Overall, more than 50% of the annual revenue comes from the US market for Sun Pharma. Incidentally, its the only plant in India from where Sun applied for product approvals for injectable drugs (apart from one such facillity in US). Thus, its also an important plant for Sun. Any clampdown (import alert) for this plant may take further 12-24 months to restore compliance standards (another Sun plant in Karkhadi, which received a US FDA import alert in 2014, is still yet to become US FDA compliant). Sun is already facing such US import bans for five of its manufacturing facilities in India.

As the present corrective steps are being implemented by Sun Pharma for the last one year, a WL means that additional effort is also required by the management for quick remediation of the same in the next twelve months. Till re-inspection is completed by US FDA, no new approvals is possible from this Halol Plant and the timing of the full resolution is quite uncertain as of now.

After steep fall in Nov on the back of this Halol Plant "legacy issues", (thanks to Ranbaxy), the scrip recovered to some extent from the bottom for various reasons and product approval of Gleevac (a block buster anti cancer drug) from US FDA may be one of them. Sun Pharma managed to shift this product to one of its US plant from the Halol. But, this may not be possible for every other product.

Technically, the scrip may be in the C-Wave (A-B-C) in the daily EW cycle and in that scenario, 1-st corrective wave in the fresh EW cycle (1-5 & A-C) may bring it again around 720 level in the days ahead. It may consolidate near 720-690-655 zone for some months until this US FDA issue is fully resolved and further clarity emerges.

But having said that, worst may not be over yet for the scrip, as the market may further discount it for any possible import alert. Thus buy in dips for Sun Pharma around 690-675 level will be better, considering the favourable risk reward ratio.

The recent US FDA WL issues with Sun & DRL also highlighted the fact that the Indian Drug Industry is still grappling with strict US standards, ranging from data integrity to quality/hygiene issues.

The recent US FDA WL issues with Sun & DRL also highlighted the fact that the Indian Drug Industry is still grappling with strict US standards, ranging from data integrity to quality/hygiene issues.

Analytical Charts:

No comments:

Post a Comment