Market Wrap: 25/10/2016 (15:30)

Nifty

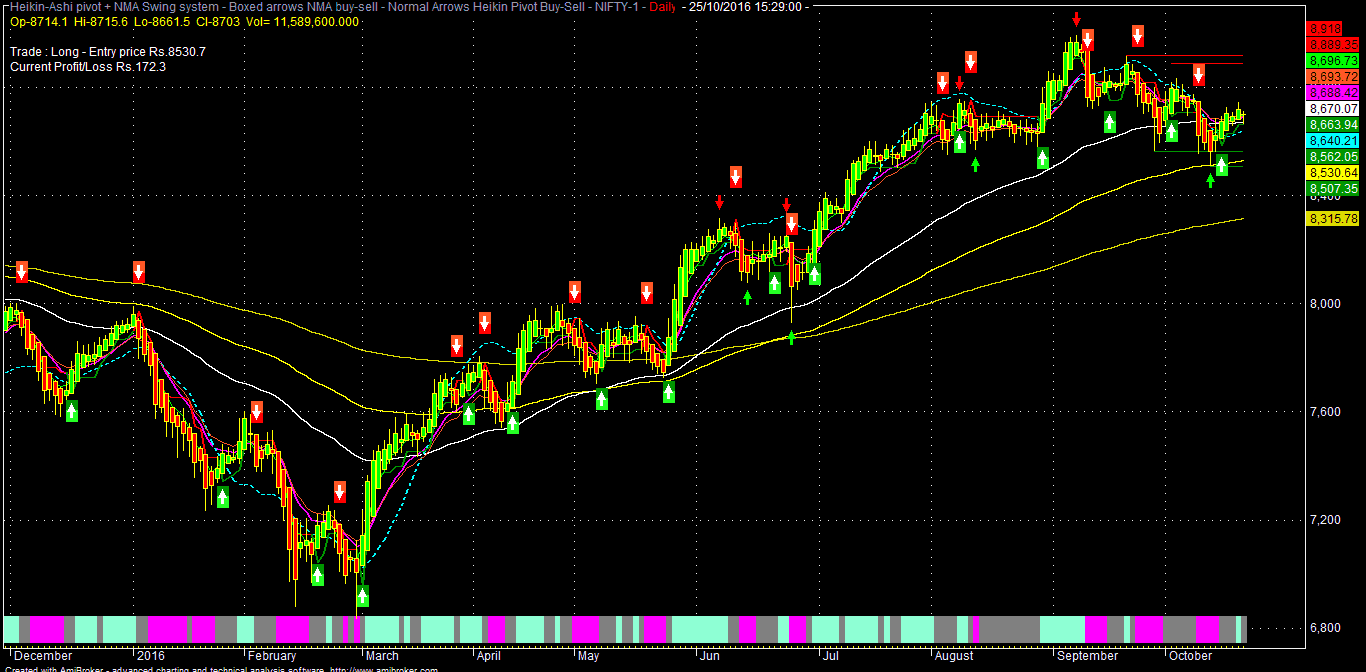

Fut (Oct) today closed around 8703 (0.20%), down by 17 points after trading

most of the days in deep negative territory as market sentiment was affected

significantly because of the surprise "Cyexit" yesterday (Cyprus

Mistry's unceremonious exit from Tata Groups).

NF

made an opening day high of around 8716 & session low of 8661.

Technically,

for tomorrow (26/10/2016), NF has to sustain over 8720 zone, for further rally

towards 8760*-8800-8840 & 8895*-8930-8995 zone in the immediate to short

term.

On

the other side, sustaining below 8695 area, NF may further fall towards

8660/8640*-8580-8545 & 8500*-8465-8405 zone in the immediate to short term.

Today,

Indian market opened almost flat following similar trend in the early morning

Asian session.

Overnight US market rallied by around 0.70% supported by better

than expected earnings & PMI data, but pressure on oil & strength in

USD capped the gain to some extent.

The overall theme was strength in dollar index on the back of recent upbeat US economic data and hawkish scripts by various

Fed speakers. FFR is now expecting around 70% probability of Dec rate hike by

the Fed. Rather than economic data, USD may be influenced now more by bond

yields difference between various G-10 currencies.

Oil was under some

pressure, because at around $50, various non-OPEC taps are opening again and

there is some skepticism about effectiveness of the OPEC's proposed production

cut plan as Iraq is raising some objection.

But, later in the day,

oil recovered again as market is awaiting for OPEC's final draft/mechanism for

the proposed production cut/freeze.

In the EU, German IFO came better than expected and together with better PMI released yesterday, market is very optimistic about the much awaited revival of growth in Germany & other parts of the EU/EZ, despite concerns of "Brexit".

In the EU, German IFO came better than expected and together with better PMI released yesterday, market is very optimistic about the much awaited revival of growth in Germany & other parts of the EU/EZ, despite concerns of "Brexit".

Today's upbeat IFO and

other economic data may be also supported by better exports to China & US,

despite another concern of stalled trade negotiation between EU & Canada.

Analysts are hopeful

for the current robust business sentiment and economic momentum to continue in

the Q4 and we may see better growth and core inflation in EU/EZ.

Although, the upbeat economic data may ease the pressure on ECB/Draghi for more stimulus immediately, it may also be a bad news for the stimulus addicted market as ECB may move towards normalization of monetary policy in the coming days (QE tapering??).

Back to home, apart from "Cyexit", Indian market sentiment may be also affected by the statement of the economic affairs secretary that GST-RNR & other rate structures and cess may be decided by next month and it’s not possible for the Govt to compensate the states for any revenue loss and running a huge fiscal deficit concurrently and thus cess is necessary on some GST rates.

Although, the upbeat economic data may ease the pressure on ECB/Draghi for more stimulus immediately, it may also be a bad news for the stimulus addicted market as ECB may move towards normalization of monetary policy in the coming days (QE tapering??).

Back to home, apart from "Cyexit", Indian market sentiment may be also affected by the statement of the economic affairs secretary that GST-RNR & other rate structures and cess may be decided by next month and it’s not possible for the Govt to compensate the states for any revenue loss and running a huge fiscal deficit concurrently and thus cess is necessary on some GST rates.

So, a GST with

multiple rates & cess may be just like another version of VAT ("old wine in

new bottle") and may serve little purpose for the expected thrust in economic

activity (GDP) and may also be an issue of less compliance.

Also, the ongoing feud in the SP & Yadav family, just ahead of UP election may cause another political crisis in the state. Some analysts believe that, in that scenario BJP/NDA may get over 150 seats in the forthcoming election in UP, which will help it for the much awaited majority in the RS (positive impact for the market).

But, some other political experts do also believe that split in SP may be more beneficial for the BSP than BJP, because of the cast & religion factor in UP. Also, as Cong is now fast becoming a "sign board" party (irrelevant in most of the states & also at the national level), regional parties are gaining fast in various states and more over, a divided SP may be more bad for the BJP rather than an united SP, which may cause more political uncertainty.

Also, the ongoing feud in the SP & Yadav family, just ahead of UP election may cause another political crisis in the state. Some analysts believe that, in that scenario BJP/NDA may get over 150 seats in the forthcoming election in UP, which will help it for the much awaited majority in the RS (positive impact for the market).

But, some other political experts do also believe that split in SP may be more beneficial for the BSP than BJP, because of the cast & religion factor in UP. Also, as Cong is now fast becoming a "sign board" party (irrelevant in most of the states & also at the national level), regional parties are gaining fast in various states and more over, a divided SP may be more bad for the BJP rather than an united SP, which may cause more political uncertainty.

Going by the present trend, in 2019 general election, various regional parties (non-BJP & non-Cong) may be a headwinds for the political uncertainty and the market, despite BJP/NDA having a better approval rate at present because of "Surgical Strike".

Yesterday, after meeting with the banks, FM hints that going forward banks may acquire more stressed assets proactively, which will be run & managed by the experienced PSU companies, having related professional expertise, specially for ailing steel, power & infra cos.

Yesterday, after meeting with the banks, FM hints that going forward banks may acquire more stressed assets proactively, which will be run & managed by the experienced PSU companies, having related professional expertise, specially for ailing steel, power & infra cos.

But, this may also be

interpreted as "back door nationalization", if implemented in reality

and may be also negative in the long run for the overall market sentiment,

although, positive for the banks in the short term.

But, ultimately actual resolution

of the NPA is necessary for the banks and not mere recognition and transfer of stressed

assets.

Indian market sentiment was also significantly affected today because of yesterday's sudden removal of Mistry from Tata Sons & various other group cos as Chairman. Subsequently, most of the Tata Group shares have fallen significantly for the concern of continuity of current strategy of deleveraging.

Indian market sentiment was also significantly affected today because of yesterday's sudden removal of Mistry from Tata Sons & various other group cos as Chairman. Subsequently, most of the Tata Group shares have fallen significantly for the concern of continuity of current strategy of deleveraging.

After Mistry's

appointment and his strategy of deleveraging & concentration on core

business having better operating margin and cash flow, various Tata group of

shares jumped significantly for the last few years. Some of the companies enjoy

better valuation multiple than its peers just because of this strategy.

Although there may be "mystery" about "Mistry"s" sudden removal and various theories are hovering around, ranging from under performance at the overall group level to TATA-DOCOMO legal fiasco & his deleveraging effort on various Tata Cos (specially Tata Steel, UK) and most importantly lack of good relation ("eye to eye") with Ratan Tata.

Although there may be "mystery" about "Mistry"s" sudden removal and various theories are hovering around, ranging from under performance at the overall group level to TATA-DOCOMO legal fiasco & his deleveraging effort on various Tata Cos (specially Tata Steel, UK) and most importantly lack of good relation ("eye to eye") with Ratan Tata.

As par some report,

the present spat started four months ago, when Tata Sons Trust (Ratan Tata)

withdrew around Rs.4000 cr form Tata Sons.

Ultimately, the board

room battle may go to court room, resulting in more chaos and uncertainty which

may affect the functioning of the board and also the morale of the present employees & key people in the Tata

Group, despite the group has an excellent HR policy.

But, whatever may be the actual reason, sudden removal of Mistry may impact the present strategy of group deleveraging efforts amid huge debts at various group cos and better utilization of capital. Various Tata group cos are now enjoying significant market (valuation) premium for this deleveraging strategy primarily employed by Mistry and those cos (Tata Steel, Tata Chemicals, Tata Comm, Indian Hotels) may be affected significantly. .

Even the cash cow TCS may be affected as market may presume that going forward, TCS has to pay more dividends/pay outs to its shareholders (Tata Sons). Sentiment of Tata Motors may also be affected, especially for the concern of continuity of various domestic strategies and existing huge debt in the consolidated books, despite good show by JLR.

But, whatever may be the actual reason, sudden removal of Mistry may impact the present strategy of group deleveraging efforts amid huge debts at various group cos and better utilization of capital. Various Tata group cos are now enjoying significant market (valuation) premium for this deleveraging strategy primarily employed by Mistry and those cos (Tata Steel, Tata Chemicals, Tata Comm, Indian Hotels) may be affected significantly. .

Even the cash cow TCS may be affected as market may presume that going forward, TCS has to pay more dividends/pay outs to its shareholders (Tata Sons). Sentiment of Tata Motors may also be affected, especially for the concern of continuity of various domestic strategies and existing huge debt in the consolidated books, despite good show by JLR.

Though, core

operations may not be affected for Tata group cos, sentiment of the investors

may be affected quite significantly. Also, rapid digitization & automation

(AI) effort for TCS may be impacted because of sudden "Cyexit" &

probable exits of his team.

Around 75% of the Tata

Group shares market capitalization may be of TCS, Tata Motors & Tata Steel

alone (all are Nifty components). Among these, Tata Steel may be worst affected

in the coming days, because of any uncertainty about its UK assets deleveraging

effort.

Also, as par some reports, Tata Sons may now aggressively expand/diversify into defense, financials & FMCG/Consumption oriented sectors and may also hold the JV/sale of Tata Steel, UK (Corus) for a target group revenue of $500 bln by 2025. Any organic or inorganic expansion may put more pressures on its balance sheets, majority of which are already stressed (except TCS) and may be more negatives for the stocks.

NSE-NF

No comments:

Post a Comment