Market Wrap: 08/03/2018

NSE-NF (March):10234 (+62; +0.61%)

NSE-BNF (Jan):24499 (+285; +1.18%)

Valuation metrics:

NS: 10243; Q2FY18 EPS: 407; Q2FY18 PE: 25.17; Avg FWD PE: 20; Proj FY-18 EPS: 418; Proj Fair Value: 8360

BNS: 24478; Q3FY18 EPS: 821; Q2FY18 PE: 29.81; Avg FWD PE: 20; Proj FY-18 EPS: 961; Proj Fair Value: 19220

For 09/03/2018:

Updated: 07:25

SGX-NF: 10280; (+46 points@0.45%)

Expected BNF opening: 24610

(Gap-up on positive global cues after symbolic metal tax announcement by Trump which is seen as less disruptive than earlier thought and an acceptance of North Korean olive branch by the US for a face to face dialogue between Trump & Kim by May’18)

March-Fut (Key Technical Levels)

Support for NF: 10240/10200-10170/10130 and 10095/10040

Resistance for NF: 10310/10350-10395/10435 and 10485/10535

Support for BNF: 24500/24200-24000/23850 and 23600/23450

Resistance for BNF: 24850/25000-25200/25400 and 25600/25850

Technical View (Positional):

Technically, Nifty Fut-Jan (NF) has to sustain over 10310 areas for a further rally towards 10350-10395 and 10435-10485/10535 zones in the short term (under bullish case scenario).

On the flip side, sustaining below 10295 areas, NF may fall towards 10240-10200 and 10170/10130-10095/10040 zones in the short term (under bear case scenario).

Technically, Bank Nifty-Fut (BNF) has to sustain over 24850 areas for a further rally towards 25000-25200 and 25400-25600/25850 zones in the near term (under bullish case scenario).

On the flip side, sustaining below 24800 areas, BNF may fall towards 24500-24200 and 24000/23850-23600/23450 zones in the near term (under bear case scenario).

The Indian market (Nifty Fut-March/India-50) closed around 10234 on Thursday, jumped by almost 0.61% and well off the day low of 10156 in late day short covering on hopes of rating upgrade by Fitch and talk of bond market intervention by the government/RBI. Overall, global cues were also supportive in hopes of less disruptive metal tax plan by Trump.

On Thursday, the Indian market opened around 10217, gap-up on positive global cues and soon came under selling pressure and succumbed to the day low amid concern of the widening impact of PNB loan fraud on the overall banking and lending & borrowing system. The market sentiment was also affected by increasing legal hurdles in the Bhushan steel auction at NCLT and tussles between various bidders, secured & unsecured creditors.

Also there was report that the Indian government is again seeking Parliamentary nod for the unprecedented 4th time in this financial year for an additional capex/spending to the tune of Rs.0.85 tln for GST compensation to the states (Rs.0.63 tln), defense pension (Rs.0.09 tln), interest payments on CMBS/T-Bills (Rs.0.10 tln). The additional spending by the government amid muted revenue collection has raised the concern of fiscal discipline again and the market came into selling pressure.

But the Indian market jumped quite smartly in the last hour of trade and made the day high of 10277 on comments by the DEA secretary Garg that they have a “good” meeting with Fitch and expecting a rating upgrade soon. Garg is also expecting another interim dividend from the RBI in this month of March (FY-18).

As par finance ministry official, the Indian government is also likely to buyback/switch GSEC/Govt bonds worth Rs.0.30-0.40 tln in the next 8-10 days, which are due to April redemption. The government is also aiming to close the FY-18 with a cash balance of around Rs.1.40 tln and is also looking for more deleverage (monetization of PSU assets) with a sustainable GDP growth around 7-8% in the coming years.

RBI may help PSBS by altering the bond category:

Also there was another market speculation that the RBI might provide one time opportunity to the banks to shift their bonds holding from AFS (available for sale) category to HTM (held to maturity) to avoid huge MTM provisions (loss) in Q4, especially for the PSBS, which are now reeling under huge MTM loss due to carnage in the Indian bond market. Almost 50% of EBITDA came from the bond portfolio and as per some reports, SBI alone is on huge MTM loss of around Rs.0.04 tln for this account alone.

This is a great news for the banks, especially for the PSBS (public sector banks) and they jumped and helped the overall market sentiment on Thursday late market hours, although it may be a temporary relief (window dressing of accounts). Indian 10Y bond yield also dropped to almost 7.655% on this unconfirmed bond market story, which may not solve the basic headwind of higher bond yields for the economy, banks, and the stock market.

As par DEA secretary Garg, the Indian government is also exploring ways to do away differential tax treatment for the FPIs/DIIs and angel investors in AIF investment (unlisted companies), so that they can raise funds without going to the bank or bond market, borrowing at exorbitant rates.

On Thursday, Indian market was helped by banks & financials (bond new boost up) automakers, media, reality, energies, infra and consumption stocks while dragged by FMCG, mixed techs (lower USD and renewed analyst optimism) metals (Trump tax tantrum) and pharma (ongoing US FDA jitters).

SGX-NF

BNF

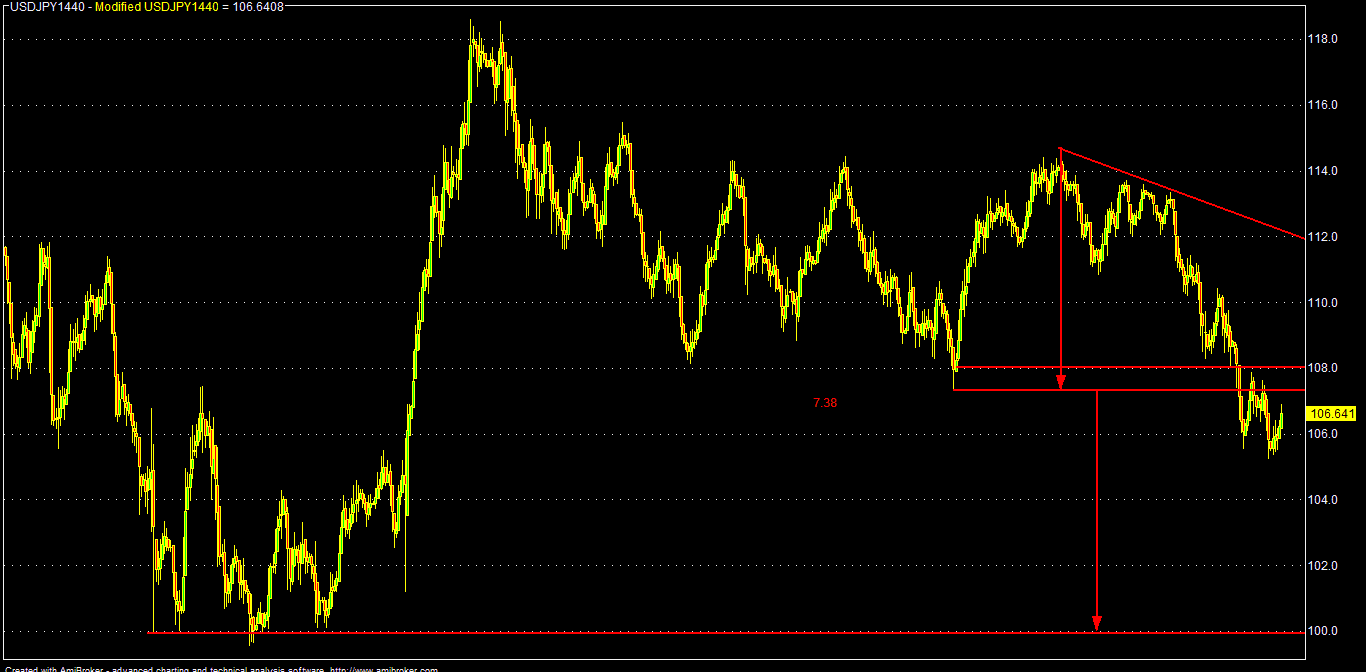

USDJPY

No comments:

Post a Comment