The stock corrected by more than 12% after the Q2 result,

which was largely inline with street estimates

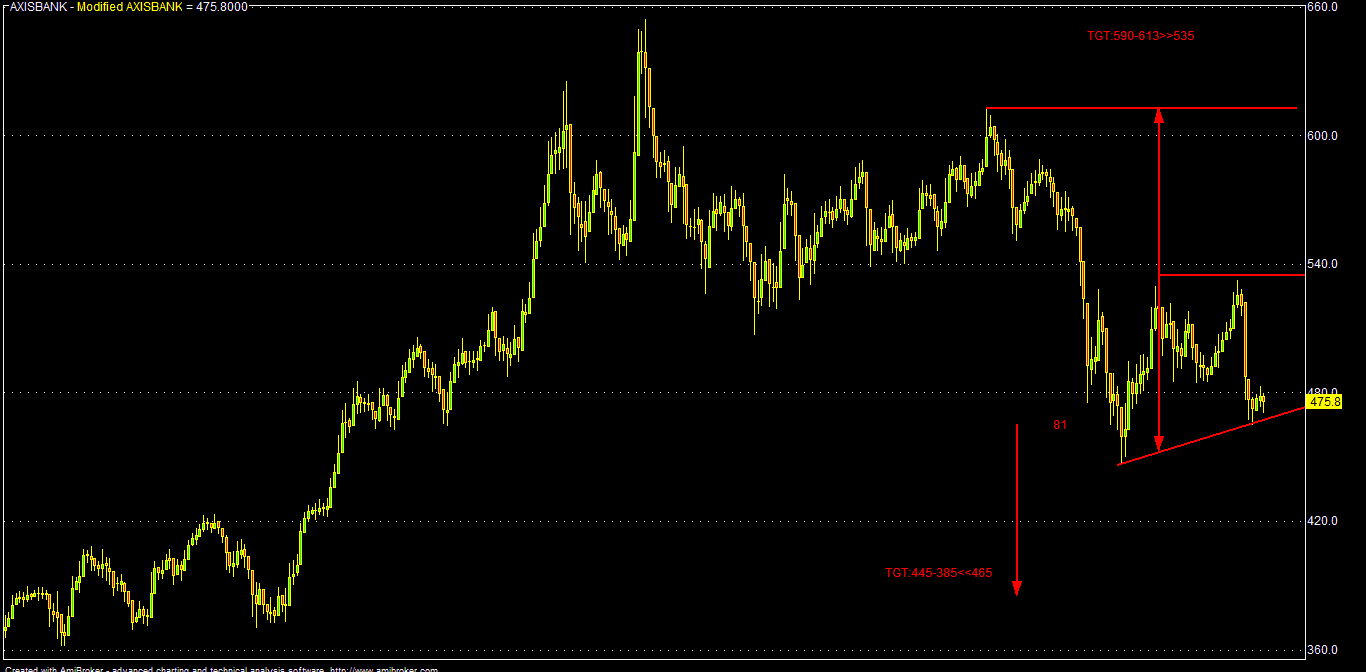

Now, 465-445 might be proved again as good demand zone for Axis Bank

For target of 535-655; Power Discoms reform might help.

CMP: 472

Buy around: 465-455-445

TGT: 490-510-535-550 (1-3M)

TGT: 590-613-655-705 (12-24M)

TSL<435

Note: For Axis, 465-445 is a strong support and 485-490 is a good resistance zone as of now. Consecutive closing below 435 for any reason, it can fall up to 415-395-375 & 355-330 area where it can be again accumulated for better investment buying average.

Some key takeaways & rationale:

Q2FY16 result and operational metrics of Axis Bank was largely inline with street estimates.

Q PAT of Axis Bank was at Rs.1916 cr, up by around 19% YOY against median street estimate of around 1912; QOQ-1978; YOY-1611.

Q2 EPS was at 8.00 against consensus of 8.22 and QOQ 8.27; YOY-6.78.

NII was also in line with market expectations and grew by around 15% YOY with a healthy loan growth of around 23%. Retail & corporate loan grew by around 26%, which may be also above industry average.

But the bank's decision to sell two power sector standard (?) loan accounts to ARC at steep discounts was thumbed down by the market.

In Q2, Axis Bank sold the above two loan accounts belonging to a same promoter group worth Rs.1820 cr for just Rs.650 cr, which caused the bank dearly for Rs.1170 cr. Out of these 1170 cr, the bank has used the Q1 contingency provision of 850 cr and made the remaining 320 cr in fresh provisions in Q2.

The bank has also refinanced another two power sector loans for Rs.1500 cr under the recent 5/25 RBI scheme. Thus fresh slippages (new stressed assets) in Q2 rose to Rs.4400 cr for Axis Bank, which is sharp incremental or sequential growth of around 83% from previous Q1 of Rs.2400 cr.

The management however retained its earlier guidance of fresh impairment (slippages) creation at Rs.5700 cr for FY-16, but this amount does not include sales to ARC(s).

Analysts are surprised because of this selling of "so called" standard loans (in Q1) to ARC at such steep discount all of a sudden in Q2.

Market is also worried about the corporate governance, transparency of the management of Axis Bank which is the the third largest private sector bank in India as these sale of standard loans was not disclosed separately in its initial Q2 earning release.

Investors seem to be loosing confidence in the credibility of management of Axis Bank and this issue of fresh slippages are also affecting scrips of other banking majors such as ICICI, SBI etc.

Market is also unhappy, because Axis Bank is not disclosing the name of the promoter group of the above mentioned stressed power sector loan accounts !! But Axis Bank may be right because of banking & client disclosure secrecy/privacy issues.

Analysts are worried over such slippages and are apprehending more similar disclosures of such stressed assets from Axis and other banks as well because of tepid conditions of power & other core sector of our economy.

But even after various ratings on the stock, the average TP for next 12M comes around 600 for Axis Bank !!

Looking ahead, with expected power sector reforms, state Govt may take the NPA(s) of state discom's on its own balance sheet !! If this happened, then it will be hugely positive for Indian banking sectors and Axis Bank may be also a major beneficiary of that.

Also, along with expected overall economic recovery to be visible by H2FY16 (?), woes of power/core sector might be diminished to a great extent. Thus formation of fresh stressed assets may be peaking as far as the core sectors of our economy is concerned because there is no "legacy issues of policy paralysis" now and Govt is also proactively taking various steps to rejuvenate this vital sector.

As par various reports, Axis Bank's has relatively low exposoure of around 2.% of its entire loan book to iron & steel sector.

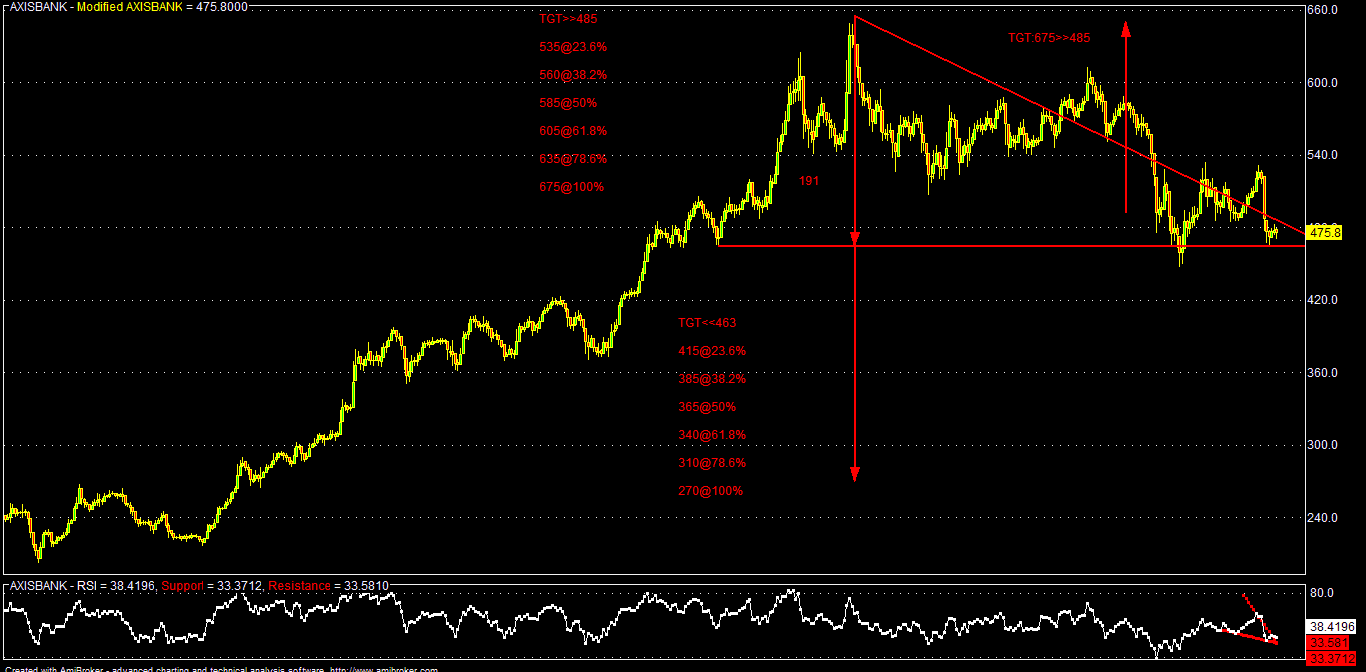

Going by the time & price action on the scrip, the above sets of bad news may be already discounted by the market to a great extent. The scrip got corrected by over 30% from early March peak of around 655, under performing the broader market quite significantly.

Looking at the technical chart, Axis Bank has strong support around 465-445 zone and its in the C Wave in monthly EW, which should be respected by the market unless we heard more about such unexpected fresh slippages. Near term target may be around 510-535.

As par BG metrics & current market parameters:

(Based on stand alone TTM & estimated forward EPS)

Present median valuation of Axis Bank may be around : 550 (FY-15/TTM)

Projected fair valuations might be around : 575-635-700 (FY:16-18/FWD)

| SCRIP | EPS(TTM) | BV(Act) | P/E(AVG) | Low | High | Median | 200-DEMA | 10-DEMA |

| AXISBANK | 33.38 | 188.02 | 18 | 557.69 | 541.23 | 549.46 | 517.64 | 487.53 |

| AXISBANK | 36.45 | 219.5 | 18 | 582.77 | 565.57 | 574.17 | 517.64 | 487.53 |

| AXISBANK | 44.55 | 255.25 | 18 | 644.28 | 625.26 | 634.77 | 517.64 | 487.53 |

| AXISBANK | 53.75 | 298.5 | 18 | 707.68 | 686.79 | 697.24 | 517.64 | 487.53 |

Analytical Charts:

No comments:

Post a Comment