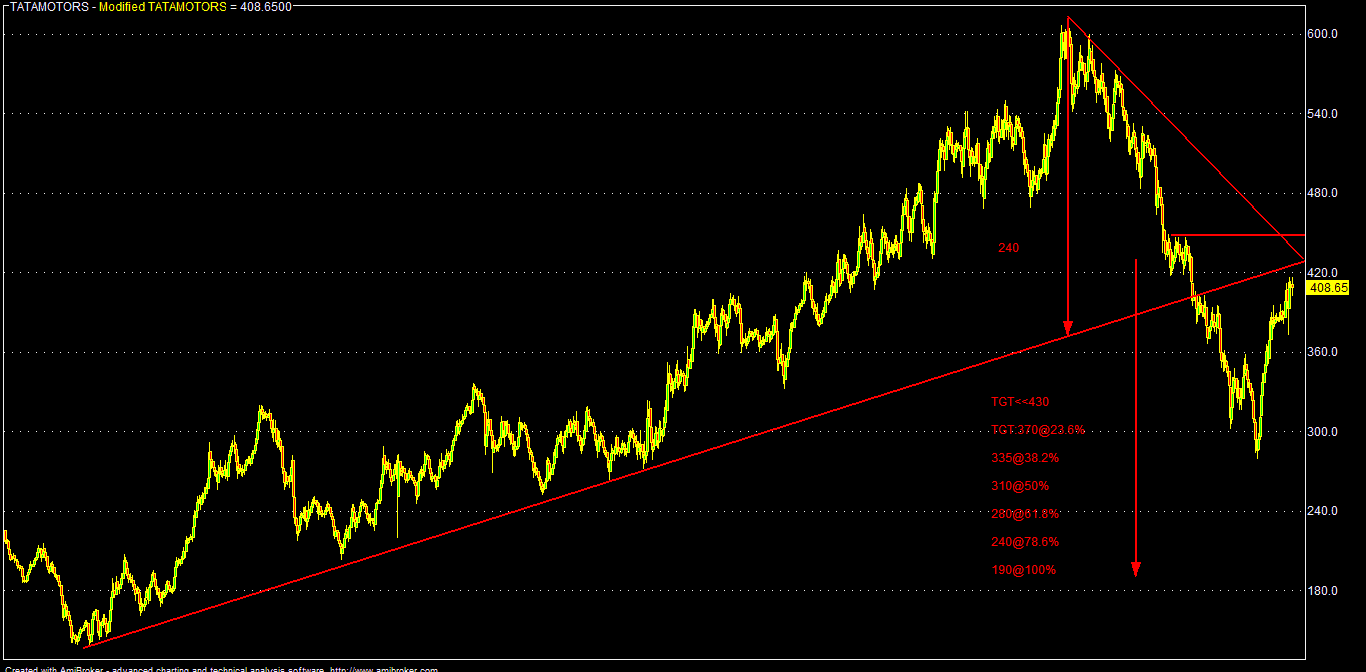

For Tata Motors 420-430 May Be Proved As A Strong Supply Zone

CMP: 404

Sell on rise near 420-430;

TGT: 395-375-350 (1-2M)

TGT: 328-308-280 (3-6M)

TSL> 440

Note: Consecutive closing above 435 for any reason, TM can scale to 448-452 zone in the near term, which is again a strong supply zone for it. Only sustaining above 452, TM may rally up to 475-492 & 510-532-575-612 zone in the mid to long term and in that scenario, "Sell" position should be reversed.

TM posts a Q2FY16 consolidated PAT of (-) Rs.430 cr (loss). The Q2 bottom line was impacted by one time loss of Rs.2493 cr on account of 5800 vehicles damaged at Tianjin port (China) explosion in JLR business. The company has filed insurance claim but due to possible delays, it has made the provision. Even, if we add this exceptional loss, Q2 PAT will be around Rs.2063 cr, which is way below the street expectations of Rs.2554 cr (YOY-3291 & QOQ-2769).

Q2 consolidated net EPS was at (-) 1.27 against YOY at 10.10 & QOQ at 8.33 (with out exceptional item Q2 EPS was at 6.57 against consensus of 5.43).

Q2 EBITDA was also down 28% (YOY) at Rs.6881 cr against consensus of Rs.9400 cr amid contraction in margin of around 4.6%, impacted by 23% increase in other expenses.

Thus Q2 result of TM disappointed the street in nearly every parameters and as par the management, poor show was due to weaker China and other EM sales which was partly offset by strong sales in UK/EU and US (North). Also robust growth (above 35% YOY) in MHICV (Medium & Heavy Commercial Vehicles) segment helped a lot in standalone/domestic (India) business.

Contribution of China (JLR) to overall global sales came down to around 18% from 27% (YOY) and this has impacted the profitability of TM to a great extent as vehicles sold in China's premium market fetch a high margin in comparison to other geographies.

Due to sluggish China market, TM was forced to relax credit terms to its dealers there and the subsequent finance cost (increase in WC requirement) has impacted the overall operating margin (OM) significantly.

TM is optimistic about revival of Chinese demand and improvement of OM in the coming quarters as auto sales volume registered a growth of around 11% last month due to Govt's stimulus there and tax cut on some automobile segment.

The management has guided sales volume of 5 lakh JLR vehicles in FY-16 amid hopes of rebounding sales in China and robust growth in US & EU. .But cross currency headwinds & weaker EUR could hurt in the days ahead.

TM will launch shortly various mid range JLR models in US, which is expected to support its volume growth

The Q2FY16 consolidated loss is the first such loss in the last 25 quarters and the total cumulative domestic loss may bar TM's eligibility in Indian defence contract as par some reports.

Standalone result of TM was also not good in Q2FY16. Q2 PAT was at (-) Rs.287.5 cr (loss) against YOY loss of Rs.1846 cr and QOQ profit of Rs.267.57 cr. (Q2 EPS was at -0.85 against YOY of -5.67 & QOQ 0.76).

Domestic performance was helped by higher operational revenue and other income but partly offset by exceptional cost. Domestic revenue was increased by 20% YOY & 12% QOQ on the back of double digit growth in MHICV segment amid continued replacement demand, moderate pre-buying and better logistics market (freight operator profitability) amid signs of overall economic recovery.

The company is very hopeful about domestic operations and is expecting an expansion in margin & EBITDA on the back of ongoing cost reduction and other margin improvement initiatives.Standalone Q2FY16 EBITDA margin was improved by around 3% on YOY basis.

Overall, domestic LCV, CV & PV unit sales (including export) declined marginally by 0.4% on YOY basis, but improved sequentially by around 8%. The company is some what pessimistic about prospect of LCV in the coming quarters because of constrained financing environment and lack of last mile load availability amid nascent industrial recovery.

But, stand alone figure is too minuscule with the overall global performance of TM and it hardly matters. Overall, Q2 numbers indicates that sales were mainly coming from EU amid low end vehicles sales and a huge depreciated EUR, which may devalue further in the coming quarters, thanks to continued QQQ by ECB and Fed talks of lift off.

The TM stock rallied by around 50% in 2 months from its Sep'15 low of around 278. This was also followed by 55% fall from its Feb'15 top of around 612.

TM posts a Q2FY16 consolidated PAT of (-) Rs.430 cr (loss). The Q2 bottom line was impacted by one time loss of Rs.2493 cr on account of 5800 vehicles damaged at Tianjin port (China) explosion in JLR business. The company has filed insurance claim but due to possible delays, it has made the provision. Even, if we add this exceptional loss, Q2 PAT will be around Rs.2063 cr, which is way below the street expectations of Rs.2554 cr (YOY-3291 & QOQ-2769).

Q2 consolidated net EPS was at (-) 1.27 against YOY at 10.10 & QOQ at 8.33 (with out exceptional item Q2 EPS was at 6.57 against consensus of 5.43).

Q2 EBITDA was also down 28% (YOY) at Rs.6881 cr against consensus of Rs.9400 cr amid contraction in margin of around 4.6%, impacted by 23% increase in other expenses.

Thus Q2 result of TM disappointed the street in nearly every parameters and as par the management, poor show was due to weaker China and other EM sales which was partly offset by strong sales in UK/EU and US (North). Also robust growth (above 35% YOY) in MHICV (Medium & Heavy Commercial Vehicles) segment helped a lot in standalone/domestic (India) business.

Contribution of China (JLR) to overall global sales came down to around 18% from 27% (YOY) and this has impacted the profitability of TM to a great extent as vehicles sold in China's premium market fetch a high margin in comparison to other geographies.

Due to sluggish China market, TM was forced to relax credit terms to its dealers there and the subsequent finance cost (increase in WC requirement) has impacted the overall operating margin (OM) significantly.

TM is optimistic about revival of Chinese demand and improvement of OM in the coming quarters as auto sales volume registered a growth of around 11% last month due to Govt's stimulus there and tax cut on some automobile segment.

The management has guided sales volume of 5 lakh JLR vehicles in FY-16 amid hopes of rebounding sales in China and robust growth in US & EU. .But cross currency headwinds & weaker EUR could hurt in the days ahead.

TM will launch shortly various mid range JLR models in US, which is expected to support its volume growth

The Q2FY16 consolidated loss is the first such loss in the last 25 quarters and the total cumulative domestic loss may bar TM's eligibility in Indian defence contract as par some reports.

Standalone result of TM was also not good in Q2FY16. Q2 PAT was at (-) Rs.287.5 cr (loss) against YOY loss of Rs.1846 cr and QOQ profit of Rs.267.57 cr. (Q2 EPS was at -0.85 against YOY of -5.67 & QOQ 0.76).

Domestic performance was helped by higher operational revenue and other income but partly offset by exceptional cost. Domestic revenue was increased by 20% YOY & 12% QOQ on the back of double digit growth in MHICV segment amid continued replacement demand, moderate pre-buying and better logistics market (freight operator profitability) amid signs of overall economic recovery.

The company is very hopeful about domestic operations and is expecting an expansion in margin & EBITDA on the back of ongoing cost reduction and other margin improvement initiatives.Standalone Q2FY16 EBITDA margin was improved by around 3% on YOY basis.

Overall, domestic LCV, CV & PV unit sales (including export) declined marginally by 0.4% on YOY basis, but improved sequentially by around 8%. The company is some what pessimistic about prospect of LCV in the coming quarters because of constrained financing environment and lack of last mile load availability amid nascent industrial recovery.

But, stand alone figure is too minuscule with the overall global performance of TM and it hardly matters. Overall, Q2 numbers indicates that sales were mainly coming from EU amid low end vehicles sales and a huge depreciated EUR, which may devalue further in the coming quarters, thanks to continued QQQ by ECB and Fed talks of lift off.

The TM stock rallied by around 50% in 2 months from its Sep'15 low of around 278. This was also followed by 55% fall from its Feb'15 top of around 612.

TM stock has a good rally amid various positive news flows recently like China automobile sales recovery, superb US growth in JLR sales numbers in Oct (by around 60%), MSCI inclusion, better car registration growth in EU etc.

Analysts are pointing out that global & China performance may be improved by better operating leverages, lower commodity prices and cost benefits from localization of production in China.

But favorable base effect of subdued commodity prices may not be there in the coming quarters as commodities might be in the process of bottoming out. There may be also some headwinds in the near term due to planned increase in Chinese dealer outlets with easy credit terms & various incentives to push sales in a subdued market.

TM is also planning to boost its domestic sales by launching various new models and gradually phasing out its existing PV/CV models (like Indigo). It is in the process of separating PV & CV segment and new PV models (like "Kite") only for personal use and not for CV. The management is planning to launch various models in Sedan & SUV segment by FY-16-19.

Clearly TM unleashes a slew of aggressive domestic PV sales revival plans and it also hired recently soccer legend Messi for its new TVC & Brand Ambassador for a face lift of "TATA MOTORS" & JLR brand globally as well as in India among the youths.

But having said that, "TATA" brand need to be branded & marketed in India more strategically as first times car buyers usually think of other brands first like Maruti/Honda/Hyundai etc rather than "TATA"; its more of a "CV" symbol here. Thus affordable models branded under "JLR" may do wonder here in India.

At the end of the day, ultimately all the efforts of the company should translate into incrementally higher earnings and unless & until that happens, TM scrip may consolidate in the near future with an eye on the Q3/Q4FY16 numbers.

The company has a huge consolidated balance sheet debt of around Rs.69000 cr as on FY-15 and D/E ratio of 1.35. Total "Tata" group debt is about 7.3 times of its total net profit as on FY-15.

Certainly huge debt is an issue with Tata groups and debt consolidation with refinancing and sale of non-core/unprofitable assets is the key going ahead. Also, being a "Tata" group, refinancing is not an issue for "TM" and TCS is also a cash flow positive company. But as a group, "TATA" is certainly paying prices of its grand & expensive acquisitions in the form of legacy issues of paying pre 2008 bull market price for the same.

No doubt, that TM

is a great stock for portfolio buying; but considering the risk reward

ratio buy on major dips near 328-308 may be

better as the above sets of news flow might be already discounted by the market to a great extent, considering its recent time & price action.

Technically, TM has strong supply zone of around 420-430 and only consecutive closing above that it may scale 452 and further upside as noted above.

As par BG metrics & current market parameters:

(On Consolidated TTM & FWD EPS)

Present median valuation of Tata Motors may be around: 450 (FY:15/TTM)

Projected fair valuations might be around: 510-555-600 (FY:16-18/FWD)

(On Consolidated TTM & FWD EPS)

Present median valuation of Tata Motors may be around: 450 (FY:15/TTM)

Projected fair valuations might be around: 510-555-600 (FY:16-18/FWD)

| SCRIP | EPS(TTM) | BV(Act) | P/E(AVG) | Low | High | Median | 200-DEMA | 10-DEMA |

| TATAMOTORS | 32.83 | 215.28 | 15 | 453.87 | 443.49 | 448.68 | 418.32 | 399.4 |

| TATAMOTORS | 41.85 | 235.75 | 15 | 512.45 | 500.72 | 506.58 | 418.32 | 399.4 |

| TATAMOTORS | 49.75 | 260.55 | 15 | 558.72 | 545.94 | 552.33 | 418.32 | 399.4 |

| TATAMOTORS | 58.5 | 292.25 | 15 | 605.87 | 592.01 | 598.94 | 418.32 | 399.4 |

Analytical Charts:

No comments:

Post a Comment