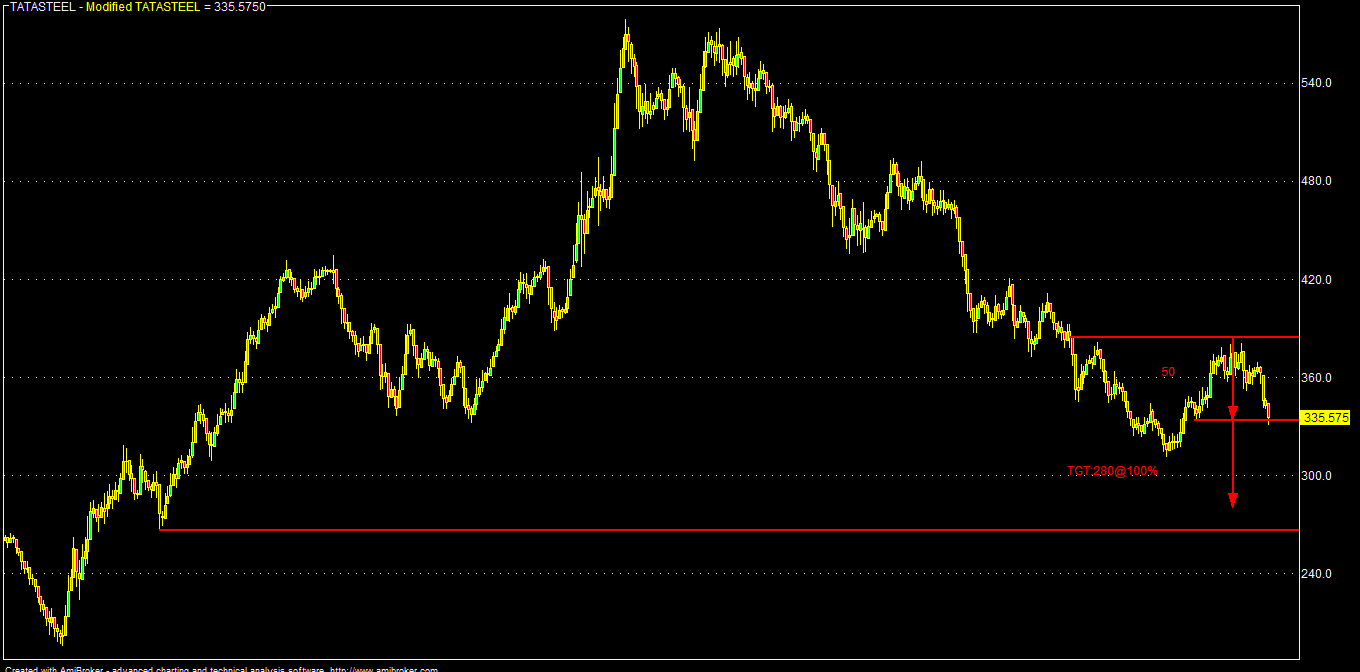

Technically, Tata Steel (CMP: 332) need to sustain over 335-340 zone to prevent any further fall. Sustain below 335, it may target 325-310 zone in the immediate to near term. Consecutive closing below 310, Tata Steel may crash to 290-280-266 zone in the bear market scenerio.

On the other hand, sustain above 340-345 zone, Tata Steel may target 355 immediately & sustain above that 366-380-385 zone may be the target in near term. Consecutive closing above 385, it may scale 398-423-435 in the medium term. In the long term, consecutive closing only above 435, it may target 580-625 (FY:17-18) in the extreme bullish market scenerio.

Bottom Line: Technical Trading Levels

| SL</>2 | FROM SLR | |||||||||

| TATA STEEL | CMP | 332 | ||||||||

| T1 | T2 | T3 | T4 | T5 | T6 | T7 | SLR | |||

| Strong > | 345 | 350-355 | 366 | 371 | 385* | 398 | 405 | 423-435 | <340 | |

| Weak < | 340 | 334-325 | 319 | 314 | 310* | 301 | 290 | 280-266 | >345 | |

Q4 earnings of Tata Steel is well below market expectations. Its consolidated net loss of 5674.29 cr includes an exceptional impairment charges of 4811.20 cr. On stand alone basis, Tata Steel's net profit fell 59% (y-o-y) to 814.09 cr. This poor result is contributed to falling steel prices, cheap imports from China & CIS, poor demand and the huge write off as mentioned above in its UK (long products) and various other overseas raw material projects. Rising regulatory costs in India also affecting its profitability and any positive value accretion from its Orissa plant is being negated by poor steel price and incremental India cost.

It appears that after the financial crisis, Tata Steel's ambitious ill timed entry into EU/UK market has not yield any positive result, either on its P&L or Balance Sheet. The company sees another tough & challenging year (2016) in EU, but expecting some rebound back home (India) amid hopes of infrastructure boom and uptick in industrial activity. It might be in the process to clean or de-leverage some of its loss making assets in EU. Combination of China slowdown & devaluation of Russian Rouble led to a surge in cheaper steel products over the last few quarters, pressuring steel prices and also squeezing Tata Steel's margin amid lackluster steel demand. Add to this, in India, a string of mining restrictions or stoppages have led to a number of its iron ore mines being shut during the past year. New MMDR bill may also enhance its cost (one time) to a great extent.

But looking ahead, all the above bad news may be already priced in in the stock price to a large extent. Worst slow down in EU & China may be over. India may also be poised to grow over 7% in the next few years, thanks to "Modinomics" and all the regulatory uncertainties for this metal sector has been cleared. Present pain of this sector, including Tata Steel may yield good fruit/result in the coming years.

As par quick BG metrics of TF model,current median valuation (stand alone basis) of Tata Steel is around 280 and projected median valuation is around 310-340 (FY:16-17) under the current market conditions (taking average PE of around 6). But, once the outlook for this metal sector improves, analysts may assign higher PE multiple of over 10-12.

| SCRIP | EPS(TTM) | BV(Act) | P/E(AVG) | LONG TERM | SHORT TERM | MEDIAN VALUE | 200-DEMA | 10-DEMA |

| TATASTEEL | 33.02 | 695.9 | 6.35 | 287.66 | 272.31 | 279.99 | 394.66 | 353.66 |

| TATASTEEL | 39.5 | 751.5 | 6.35 | 314.63 | 297.84 | 306.23 | 394.66 | 353.66 |

| TATASTEEL | 47.5 | 811.6 | 6.35 | 345.02 | 326.61 | 335.81 | 394.66 | 353.66 |

No comments:

Post a Comment