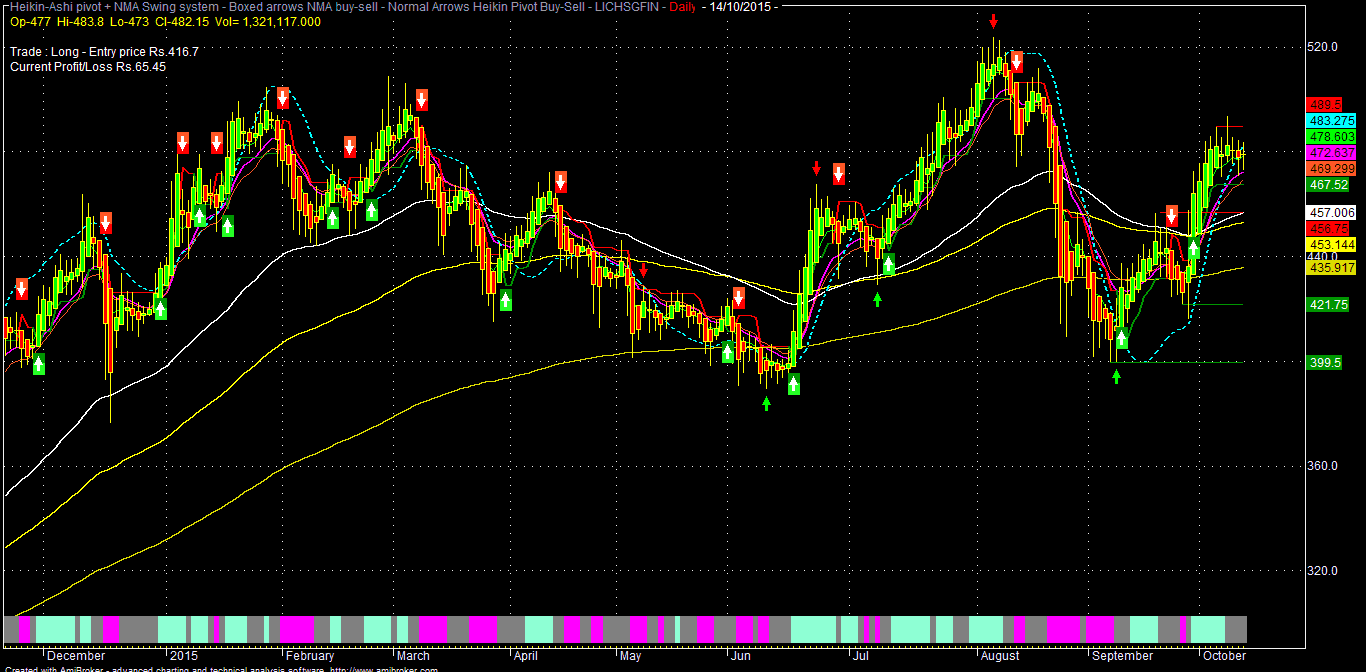

Expect 525-550 Only Sustaining Above 490-510, Otherwise Free Fall Up To 421-399 (Below 460)

Analysts are expecting Q2 PAT at around Rs.400.40 cr up by 17% (YOY) and QEPS at 7.85

CMP: 482

Buy : 478-467

TGT:490-510-525 (T+5)

TGT: 550-650-720 (1-24M)

TSL<460

Note: Consecutive closing below 460/450 for any reason, LHFL can fall up to 421-399-375 level, where it may be accumulated again for better investment buying average.

Some Key Takeaways:

Market is expecting somewhat steady growth in earnings due to sequentially lower cost of funds (better NIM) but might be pulled down to some extent for higher provisions.

Housing finance companies (HFC), such as LHFL, HDFC rallied considerably since 29-th Sep (RBI policy date) because there was a proposal for reduction in risk weightage of lower value but well collateralised individual home loans (up to Rs.35-75 lacs) for the "affordable housing" theme /push by the Govt. This may translate for more home loans by the HFC(s) with their existing capital.

Market will also keenly watch composition of LHFL's loan book which has increasing mix of developer's loan along with retail & LAP, trend of NIM, loan growth and asset quality (NPA).

But considering the recent price action, the scrip is trading close to its vital resistance (supply) zone of 490-510 and only above estimate result and upbeat management commentary (guidance) will be able to break these technical hurdle for new high towards 550 in the coming days.

LHFL is the 2-nd largest housing finance co in India and has wide distribution network with backing of a trusted PSU brand like LIC (which has around 40% stake in LHFL). It is also a strong contender of some form of Banking License by RBI in future.

Looking ahead, with the "smart city theme" and "affordable housing for all" thrust by our Govt coupled with lower interest environment and 7-th pay commission induced liquidity, a HFC like LHFL should be one of the major beneficiary and investors may buy in dips taking the opportunity of any result oriented volatility.

As par BG metrics & current market trends:

Present median valuation of LHFL may be around: 550 (FY:15)

Projected fair valuations might be around: 600-655-710 (FY:16-18)

| SCRIP | EPS(TTM) | BV(Act) | P/E(AVG) | Low | High | Median | 200-DEMA | 10-DEMA |

| LICHSGFIN | 28.65 | 154.92 | 23 | 535.96 | 558.07 | 547.02 | 435.92 | 472.64 |

| LICHSGFIN | 33.95 | 19.55 | 23 | 583.43 | 607.50 | 595.47 | 435.92 | 472.64 |

| LICHSGFIN | 41.05 | 22.25 | 23 | 641.54 | 668.01 | 654.78 | 435.92 | 472.64 |

| LICHSGFIN | 48.25 | 25.35 | 23 | 695.53 | 724.23 | 709.88 | 435.92 | 472.64 |

Analytical Charts:

No comments:

Post a Comment