The stock jumped almost 13%;

Now expect 300-350 only sustaining above 287

Now expect 300-350 only sustaining above 287

Q2 PAT at Rs.116.41 cr up by around 23%

(expectation 105; YOY-94.81; QOQ-90.27)

(expectation 105; YOY-94.81; QOQ-90.27)

Q2 EPS at 2.45

(expectation 2.21; YOY-2.00; QOQ-1.90)

(expectation 2.21; YOY-2.00; QOQ-1.90)

CMP: 277

Buy either breakout above 287 or in dips around:255-245

TGT: 287-300-325 (1-3M)

TGT:350-450 (12-24M)

TSL<236

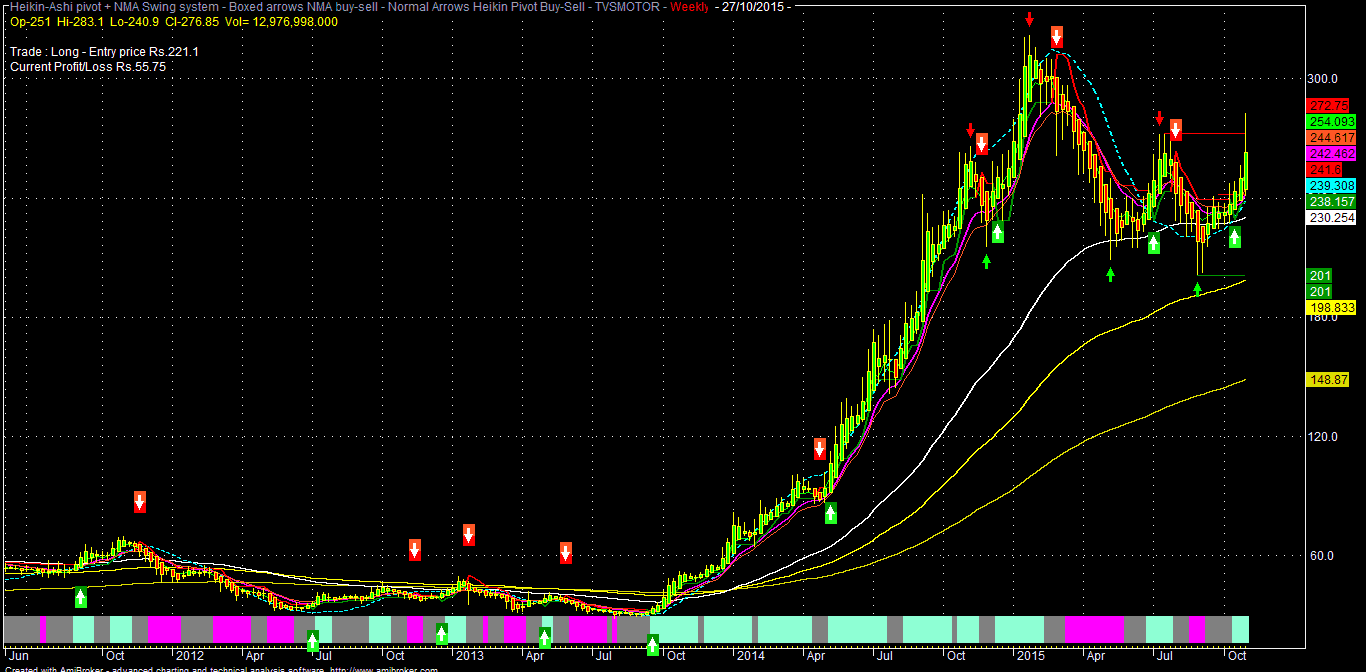

Analytical charts:

TGT: 287-300-325 (1-3M)

TGT:350-450 (12-24M)

TSL<236

Note: For TVS, 272 is now a strong support and sustain below 272, it may again fall to 255-245 zone, where buying may be initiated. Consecutive closing below 236, it may further fall to 230-224-213 & 207-201-195 zone, where one can again accumulate for better buying average, depending on the overall news flow and market sentiment.

Some key takeaways & rationale:

TVS yesterday surprised the market with its Q2FY16 result, which is significantly higher than analysts consensus..

The excellent result is primarily due to better product mix and lower raw material cost amid depressed commodity prices (steel/rubber etc) and also by better vendor negotiations, which led to improved operating margins too.

Although, overall 2-W sales in absolute units fell YOY, its Scooter sales (mainly Jupiter) grew by almost 12% and exports rose by 23%.

Net realization per vehicle grew by more than 7% above estimates also.

Going ahead, the company is optimistic about ongoing festival season sale and depending mainly on its blockbuster Jupiter brand of Scooty for the same.

Recently, its also hired legendary mega star Amitabh Bachchan for its Jupiter & other TVS brands ad.

TVS is not going to launch any new product in the current festival season and will concentrate on the existing models. It may launch new models in FY-16 onwards.

The company is eyeing around 18% market share by FY-16 from present 13%.

TVS is now emphasizing more on better margin 2-W & 3-W and less on moped sales.

Almost all the analysts gave "thumbs up" to the excellent Q2 result of TVS, considering that its the only domestic 2-W company, which is consistently growing along sustained volume and able to meet the competition from the mighty of Honda (specially Activa scooty).

Now, considering all the above good news for TVS, the scrip already reacted already rallied around 13% and 18% (from day low to day high) in one day !!.

Looking at the chart, TVS now has to sustain over 287 for its next target of 300-325 in the near term with 272 being the crucial technical support.

Sustain below 272, it may got corrected to some extent towards 255-245 zone, where we may see again good buying interest.

As par BG metrics & current market parameters:

Present median valuation of TVS may be around: 245 (FY:15/TTM)

Projected fair valuations might be around: 280-330-375 (FY:16-18/EST)

| SCRIP | EPS(TTM) | BV(Act) | P/E(AVG) | Low | High | Median | 200-DEMA | 10-DEMA |

| TVSMOTOR | 8.16 | 34.63 | 30 | 240.36 | 246.80 | 243.58 | 236 | 248.81 |

| TVSMOTOR | 10.55 | 40.75 | 30 | 273.30 | 280.62 | 276.96 | 236 | 248.81 |

| TVSMOTOR | 14.75 | 47.25 | 30 | 323.16 | 331.81 | 327.48 | 236 | 248.81 |

| TVSMOTOR | 19.25 | 54.9 | 30 | 369.17 | 379.06 | 374.12 | 236 | 248.81 |

Analytical charts:

No comments:

Post a Comment