Transforming itself into digital model (semi e-commerce)

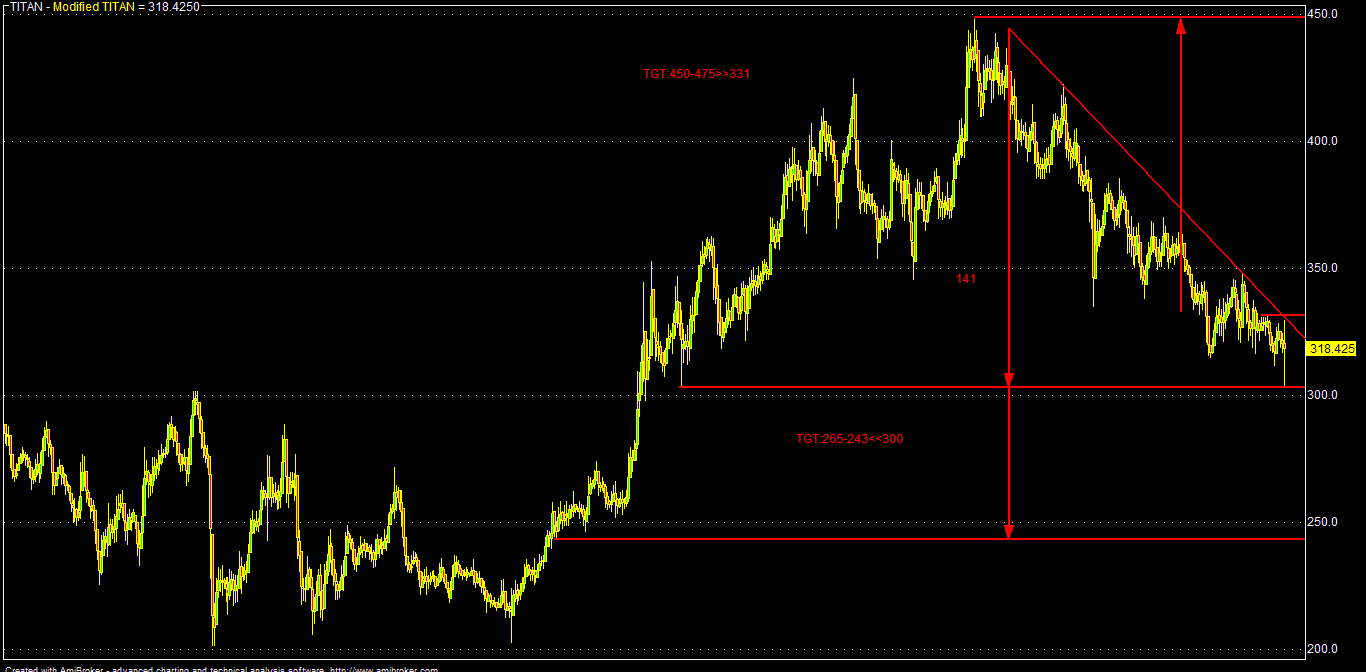

CMP: 327

Buy either on sustained breakout above 331 or wait for dips around 302-288

TGT: 370-450-475 (1-12M)

TGT:525-600 (24-36M) (Only sustaining above 450)

TSL<280

Note: Consecutive closing below 280 for any reason, Titan might fall up to 260-240 zone, where it can be again accumulated for better buying average (investment purpose).

Titan suffered nearly 30% correction from its Feb'15 pick of around 448 in the last eight months against overall recent market corrections of around 12%.

Some of the reasons behind it may be: (As par management's own view)

- The deep discounting model of e-commerce players.

- Weak consumer sentiment, specially in the rural & urban middle class people.

- Withdrawal of "Golden Harvest" scheme by the company due to poor rural wedding season demand (for Jewellery & Watches).

- Prolonged weakness in the gold prices.

- Cross currency headwinds & cheap import of jewellery (legal or illegal).

- Intense domestic competition from other jewellery, eye-wear and watch makers (both organized & unorganized players).

- Recent trend of i-Watch among young tech savvy consumers.

Looking forward:

- Titan is planning is digital foray into e-commerce and will launch it shortly with appropriate strategy by expanding its physical stores for better consumer preferences.

- All e-commerce players are in deep discounting model using its own equity capital !! Certainly this model will not survive and creating a bubble which can burst any time. Already, they are slowly reducing their discounts on various items.Almost all retail e-commerce players in India are still making huge loses. At some point of time, investors will want to see "money" (profit).

- Titan is also in the process to launch semi version of i-Watch (smart watches like i-Phone).

- The company is also diversifying into other related consumer goods like fragrance etc into semi-premium category.

- Various regulatory concerns regarding gold import policy is reducing and gold supply is gradually improving now. Thus coupled with relatively cheap gold prices and reduced making charges, demand for jewellery should improve sequentially higher with forthcoming festival and wedding season.

- Both Gold & USDINR should be in a predictable range as Fed will be in no hurry to hike interest rates in near future (Max: 0.25-0.50% in FY-16).

- Due to expected economic recovery in FY-17 & 7-th pay commission in Jan'16, overall discretionary consumer spending may increase sequentially higher and Titan could be a beneficiary of that also.

Thus, considering all the above pros & cons and recent corrective price action of the Titan scrip, it may be a good investment as risk reward ratio is favorable.

As par BG metric, valuations of Titan (in the current market parameters):

Current median value may be around: 330 (FY: 15)

Projected fair valuations might be around: 355-385-425 (FY:16-18)

| SCRIP | EPS(TTM) | BV(Act) | P/E(AVG) | LV | SV | MV | 200-DEMA | 10-DEMA |

| TITAN | 8.98 | 34.83 | 35 | 333.66 | 318.22 | 325.94 | 354.21 | 322.18 |

| TITAN | 10.5 | 158.25 | 35 | 360.79 | 344.09 | 352.44 | 354.21 | 322.18 |

| TITAN | 12.25 | 221.55 | 35 | 389.70 | 371.66 | 380.68 | 354.21 | 322.18 |

| TITAN | 15 | 310.15 | 35 | 431.23 | 411.27 | 421.25 | 354.21 | 322.18 |

Analytical Charts:

No comments:

Post a Comment