Market Wrap: 22/12/2017 (17:00)

NSE-NF (Dec):10505 (+43; +0.41%)

(TTM PE: 26.84; Abv 2-SD of 25; TTM Q1FY18 EPS: 391;

NS: 10493; Avg PE: 20; Proj FY-18 EPS: 418; Proj Fair Value: 8360)

NSE-BNF (Nov):25676 (+55; +0.21%)

(TTM PE: 29.58; Near 3-SD of 30; TTM Q1FY18 EPS:

867; BNS: 25649; Avg PE: 20; Proj FY-18 EPS: 961; Proj Fair Value: 19220)

For 26/12/2017: Dec-Fut

Key support for NF:

10425/10375-10315/10250

Key resistance for NF:

10525/10550-10600/10640

Key support for BNF: 25600/25400-25200/24950

Key resistance for BNF:

25775/25875-26050/26200

Trading Idea (Positional):

Technically, Nifty Fut-Dec (NF) has to sustain over 10550 area for further

rally towards 10600/10640- 10695 & 10745-10795 zone in the short term

(under bullish case scenario).

On the flip side, sustaining below 10525 area, NF may fall towards 10490/10425-10375/10315

& 10250-10190 zone in the short term (under bear case scenario).

Technically, Bank Nifty-Fut (BNF) has to sustain over 25775 area for further

rally towards 25875- 26050 & 26200-26325 zone in the near term (under

bullish case scenario).

On the flip side, sustaining below 25725 area, BNF may fall towards

25600/25400-25200/24950 & 24850-24700 area in the near term (under bear

case scenario).

Indian market (Nifty Fut-Dec/India-50) today (22nd Dec) closed around 10505, soared by almost 43 points (+0.41%)

and made an opening session low of 10456 and late day high of 10515 as “Santa

Rally” extended on the X-Mas weekend; Nifty spot made a fresh life time high of

10501 and made a fresh life time high today in line with “global trend” of

“Goldilocks rally”.

Indian Market Celebrates X-Mas By Another Milestone

High:

Indian market today opened around 10460, almost

flat on positive Global/Asian cues and domestic optimism about Govt’s fiscal

stimulus to revive the rural economy after disappointing result in the recent

GJ election, where rural voters has basically shunned the Govt/BJP for un/under

employment issues and DeMo & GST blues.

Market lost some momentum on soft EU market

opening today but soon gained strength on optimistic

outlook for the Indian economy in 2018 by IMF & Govt assurance that there

will be no closure of any stressed PSB and recaps plans are on the track.

As par IMF, “DeMo & GST brought short-term pain but

long-term benefits; Expect growth in India to be 6.7% this year (2017) &

7.4% next year (2018); India not growing as fast as the rest of world is an

aberration; GST is a work in progress but the economy is adjusting to it; See

growth gradually increasing in the next fiscal year; Costs of DeMo are

temporary; See permanent & substantial benefits due to DeMo; Govt has taken

very important first steps to resolve the NPA problem”.

IMF- “IBC has prompted the world bank to raise the ease of doing

biz score of India; PSU banks need more from the Govt in the form of reform; India

has done a lot wrt opening up of foreign direct investment”.

Although IMF is very optimistic, slow pace of resolution of

India’s huge corporate NPA/NPL may be a big headwind and the economy needs to

grow by over 8%, if not in double digit to generate adequate quality jobs to

the vast pool of educated & skilled young work force.

Market gained further momentum & scaled new high after RBI

assured that “reports of closure of PSBS under corrective action are wrong”;

Govt also came forward and clarified that “no question of closing down any

Bank; Govt is strengthening PSBS by Rs.2.11 tln recapitalization plan; do not

believe rumour mongers; Recap, Reforms roadmap for PSBs firmly on track”.

But market need to justify its extremely stretched valuation in

the coming days as at 10500, Nifty TTM PE is around 26.85 on reported TTM EPS

of 391; this is far high from historical average PE of 20-18 despite power of

liquidity, especially domestic EQ/MF flows.

Previously, market was assuming FY:

18-19 Nifty EPS around 475-525, but considering the present trend and macro

situation, GST & DeMo spillovers, FY-18 EPS may come around 418 eventually;

all eyes will be now on FY-19 budget & Q3FY18 earnings,

Market may be also in dilemma of fiscal stimulus & deficit

in the coming days amid talks of rural centric budget for FY-19, keeping an eye

on the forthcoming series of state elections in 2018; it will be the last full

fledged budget by the Govt/BJP before going into the early 2019 general

election, which may be also fought closely after encouraging result from GJ for

INC.

A higher Indian bond yields, now hovering around 7.30% and

eyeing for the 7.50% milestone may be also a headwind for the Indian corporates

& economy, being almost 5% higher than US bond yields; cost of funds may be

significantly higher for the Indian corporates not only domestically, but also

for the foreign fund raising amid stressed B/S.

Moreover, US tax reform and cut in corp tax & tax on foreign

assets/profits/repatriation issues may prompt all the other countries including

India to offer similar corp tax package to prevent outflows and this may also

affect the revenue side significantly in the coming days. Thus fiscal math may

also be in disarray coupled with surging Oil and GST disruptions despite

increasing thrust on disinvestments.

Revenue from telecom may be also in pressure, while Govt is

planning another pay bonanza for its employees. Govt has to spend more on its

capex to keep Indian growth story intact as private capex is still muted; the

same is true for private consumption.

Today Nifty was supported mostly by Infy, TCS (renewal of

contract with its US client Nielson and upbeat earnings from Accenture), RIL

(analysts optimism) Bajaj Fin, ONGC (higher Oil), HDFC Bank, SBI, HDFC, Maruti

and L&T by around 44 points altogether, while it was dragged by Ultratech

Cement, IOC, DRL, Tata Steel, VEDL, Indusind Bank, HCL Tech, Lupin, Hero Motor

& Auro Pharma by almost 8 points cumulatively.

Overall, today Indian market was supported by banks &

financials, auto, techs, media, FMCG, reality, consumptions, energies &

infra, while it was dragged by metals, selected pharma, OMC slightly.

SGX-NF

BNF

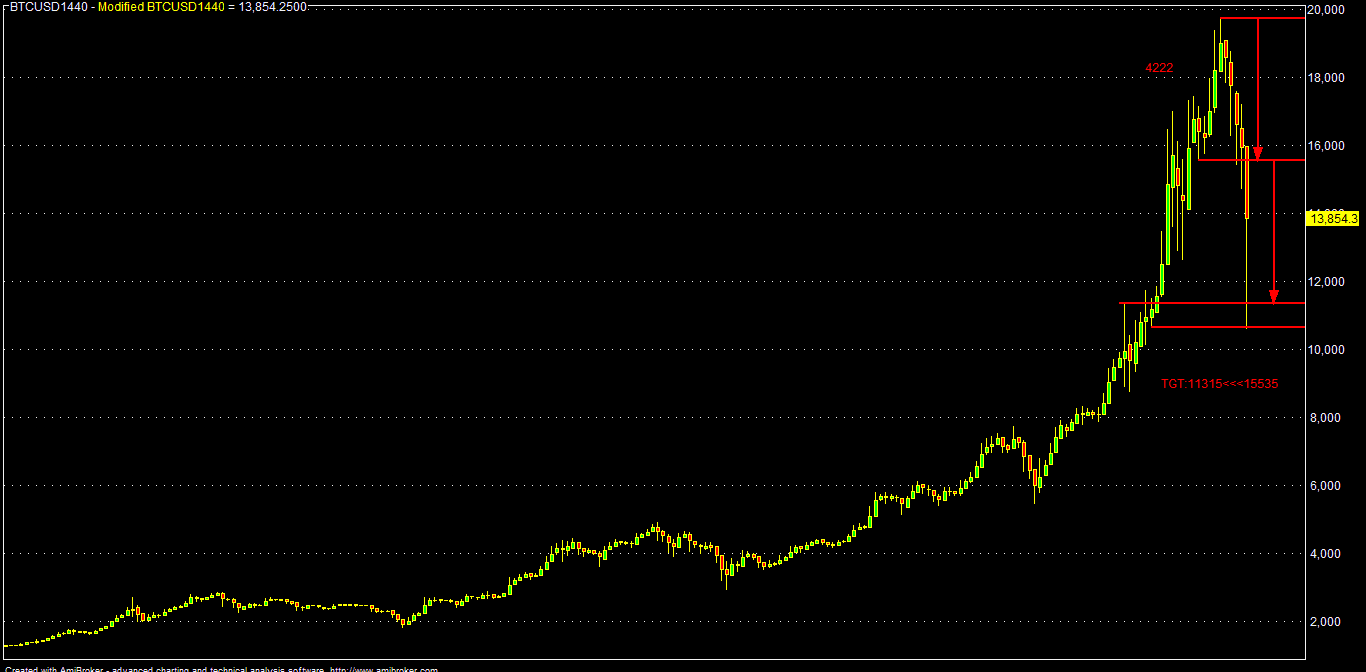

BTCUSD

No comments:

Post a Comment