For NF, consecutive closing above 7560-7625 zone, expect further rally up to 7775-8005;

Otherwise, we can see some selling pressure;

and sustain below 7470, NF can again fall towards 7300-7005 area.

Trading Levels: Nifty Fut (Mar)

SGX NF: 7532 (CMP)

NSE-NF: 7475 (LTP)

| SL (+/-) 10 POINTS | FROM SLR | |||||||

| For | Intraday Swing | Trader | ||||||

| T1 | T2 | T3 | T4 | T5 | SLR | |||

| Strong > | 7560 | 7595-625* | 7645-695 | 7715-775* | 7800-825 | 7860-885 | <7540 | |

| Weak < | 7540 | 7505-470* | 7430-385 | 7350-300* | 7275-230 | 7200-135 | >7560 | |

| FOR | Conservative | Positional | Trader | |||||

| T1 | T2 | T3 | T4 | T5 | SLR | |||

| Strong > | 7560 | 7625* | 7695 | 7775* | 7825 | 7885-8005 | <7540 | |

| Weak < | 7540 | 7470* | 7385 | 7300* | 7230 | 7110-7005 | >7560 | |

Our market rallied last week quite smartly amid massive short covering on the back of positive global market trends (China RRR cut & further PBOC/ ECB/BOJ stimulus hope and positive US data) coupled with not so-much negativity in the budget (no LTCG, but DDT there) and some positive surprise (Govt. sticking to 3.5% of fiscal deficit for FY:2016-17) in the 2016 budget.

Govt has reported estimated FD @3.9% of gross GDP for FY-16 (against 3.7% of earlier target) and gave a projection of 3.5% for FY-17 and 3% for FY-18. Market was expecting a higher FD of around 3.7-3.9% for the same and this has caused the short covering rally along with DDT factor.

To avoid DDT (a triple tax on corporate profits ??) from the next FY, majority of high dividend paying companies are announcing special/interim dividends pay out in March'16 and this has also caused a huge buying in to spot market and NS is trading at significant premium of around 40 points wrt to NF !!

But the excessive dividend pay outs in this FY to dodge the Govt's DDT plan (which is also very regressive) for the HNI/institutional shareholders (having annual dividend income above Rs.10 lacs), may also hurt the cash flow for the next FY and it may also showing that many companies has no plan for business expansion/diversification and thus are returning excess cash to its share holders either through special dividends or buy back. This is again an indication that corporate India is now running through excess capacity and tepid demand.

Market is expecting an out of policy date rate cut (0.25%) by RBI amid Govt's projection of 3.5% FD and fiscal prudence backed by lower capex of the Govt (which may led to lower borrowings by the Govt and ease pressure on the liquidity and rate side). But, going by the recent RBI commentary, it may act only on the policy date (5-th Apr) and the current rally may already discounted 0.25% or even 0.50% rate cut.

Market is also expecting that like last year, RBI may jump with a 0.25% rate cut as a "Holi Gift to the nation", after seeing the Fed/ECB/BOJ action in the next two weeks.

Apart from DDT & 3.5% fiscal deficit target for FY-17 some other key proposals of the 2016 budget:

1. Increase of STT on sale of stock options from 0.017% to 0.05% (no impact on investors).

2. Non imposition of DDT on REITS.

3. Service tax on telecom spectrum.

4. Luxury tax on vehicles priced above Rs.10 laks.

5. EV tax/cess on certain category of vehicles.

5. Ad-valorem tax (20%) on domestic crude oil (much higher than the market expectation).

6. No LTCG and increase in Service Tax as feared by the market.

7. Increased rural (10%) and infra & energy (35%) sectors capex.

8. Increased income tax benefit for low cost housing and house rent, but came with many riders too.

9. Allocation on recapitalization of the PSBS is highly disappointed as Rs.25000 cr is provided against market expectation of Rs.40000 cr.

10. An infra cess (1-4%) and farmer's welfare cess (0.5%) on all taxable services against market expectation of 1.5% hike in service taxes (in line with the proposed GST rate roadmap).

11. Tobacco ED increased by 10-15% (depending on lengths of Cigarettes).

12. GAAR will be implemented from FY-17 in line with the previous announcement by GOI in 2015.

Majority of the analysts are describing this 2016 budget as "neutral to negative" as there is a question mark about the "investment boosting" capability of this budget. In the absence of any meaningful private investment amid highly stressed corporate balance sheets with tepid consumer demands, all are looking to the Govt for a meaningful ramp up of public investments as in the present scenario, its the Govt, which can borrow from the market at the lowest possible rate.

Market was expecting that Govt may increase its capex significantly, even at the cost of some fiscal deficit numbers. But neither happened and the reported/projected fiscal deficit number (3.9-3.5%) is also looked doubtful as some projected revenues might be overstated whereas some expenditure may also be understated. Also, the 11% projected growth in nominal GDP too looks like on the higher side in FY-17 against the RE of 8.6% at FY-16.

Regarding 3.5% projected fiscal deficit number, there are definitely some doubt about the assumed disinvestment and telecom spectrum revenue (irrational high) and full impact of 7-PC/OROP and proper accounting of pending food & fertilizer subsidy bill (only 40-50% may be accounted, while the GOI is saying that now, 60-70% of 7-PC is accounted in the budgetary projection).

Majority of the analysts are apprehending some more correction in the near term due to the disappointment in the budget, highly stressed balance sheets of the corporates, NPA mess of the Indian Banking System (specially PSBS), earning downgrades, rising political turbulence and non-passage of vital reform bills in the RS, growing disapproval in NAMO and some kind of lost of faith in "Modinomics" etc along with current global market turmoil (specially Oil and China slow down and fear of further Yuan devaluation).

Global market is looking for some form of more stimulus (QQE) from major central bankers in the coming days.

ECB is expected for a (-) 0.01% rate cut to bring it at (-) 0.4% (NIRP) and an increase in the QE programme for EUR 75 bln from the present 60 bln purchase/month and extend the time of the same from March'2017 to at least March'2018 (ECB date: 10/03/2016).

If Draghi come with a "water pistol"instead of a "bazooka", then risk assets will be sold again.Considering the neutral stance & hawkish script of FED and its "wait & watch" policy, Draghi may come with a "pistol" only (i.e. only 0.01% rate cut without any additional QE) this time and keep his "bazooka" arsenal ready for the next FED meeting/action in June-Dec'16.

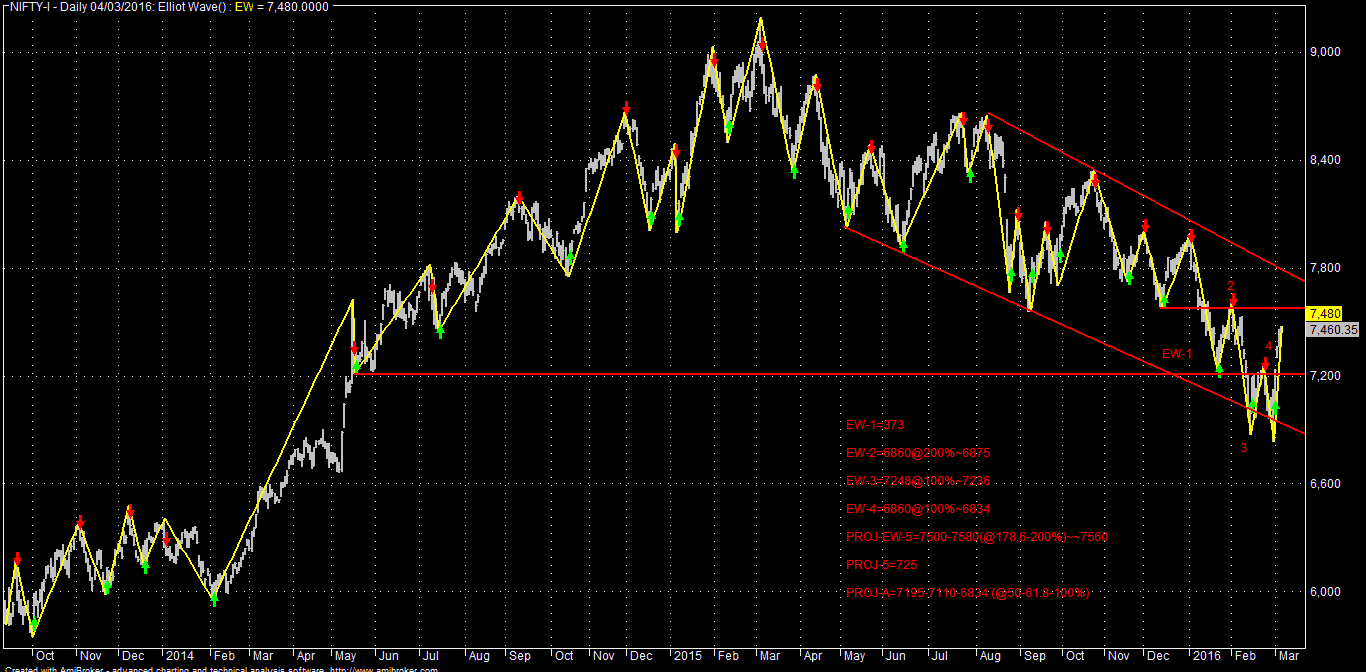

Looking at the chart, NF may be in the 5-th wave of daily EW cycle and the extended target of the same may be around 7500-7580 zone. In that scenario, the next corrective A-wave can bring it towards 7195-7110 & 6834 area. Only consecutive (3 days) closing above 7625 will invalidate this scenario and in that case, NF may further rally up to 7775-8005 zone in the near term.

Technically, SPF (CMP: 2000) after 11% rally from the 1804 bottom in the last two weeks, now has to stay above 2008-2016 for further rally up to 2075-2095-2110; otherwise it will again fall to 1971-1946-1907 area.

Analytical Charts:

No comments:

Post a Comment