Trump

rally may be too fast and much ahead of reality; US market may correct in

Jan’17.

Trade

protection & higher fiscal spending rhetoric by Trump may cause significant

upper trajectory in US inflation and subsequent stronger USD may also result

into a significant earnings erosions for US corporates, despite perception of

“Trumponomics” (higher spending, lower tax, higher corporate profits and higher

job creations; higher inflation & higher growth).

2017

may be a year of some serious geo-political risks not only for EU, but may also

be for US itself (an unpredictive and politically inexperienced President with

a cabinet or main advisors, some of whom may have conflicts of interests

because of their own business empire and a known China hawk).

Global Mantra Part-II:

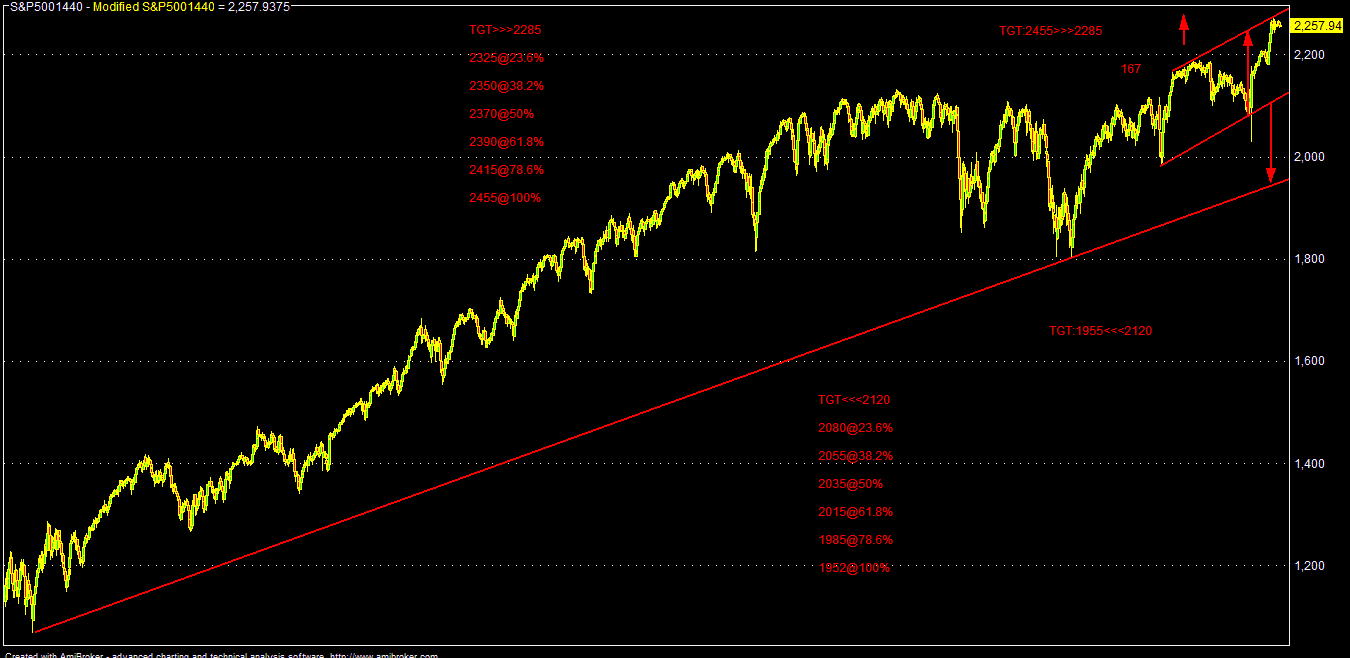

24/12/2016 (11:30)

SPX-500 Fut: 2259 (LTP)

Technically,

SPX has to sustain over 2285-2305 area for any further rally towards 2315-2350

& 2390-2420 and 2455-2510 zone in 2017; i.e. it may have further upside of

around 8-10% from its recent high of around 2273 (under bullish case scenario).

On

the down side, sustaining below 2275-2255 area, SPX may further fall towards

2240-2210 & 2190-2165 and 2140-2120 zone in the near term (3-6 months);

i.e. it may correct by around 5-7% from its recent high of around 2272 (under

bear case scenario).

DJI-30 Fut: 19859 (LTP)

Down

Jones Fut (DJ-30) has to sustain over 20100-20250 area for any further rally

towards 20450-20750-20900 & 21150-21400-21800 and 22250-24150 zone in 2017;

i.e. it may have further upside of around 12-20% from its recent high of 19917

in the bullish case scenario.

On

the down side, sustaining below 19975-19825 area, DJ-30 may further fall

towards 19700-19400-19000 & 18750-18550-18295 and 17750-17400 zone in the

near term (3-6 months); i.e. DJ-30 may correct by around 10-13% in the bear

case scenario.

In

2016, SPX rallied by around 11.5% & 26% from the Feb’16 low and more over

12% alone from “Trumpism Day” low. Similarly, DJ-30 rallied by over 14% from

“Trump day” (9th Nov) low on the back of relentless rally after

initial “epic fall” as “President” Trump sounds different against earlier

election rhetoric of “Candidate” Trump. His carefully crafted election victory

speech that “We will rebuild America” and conciliatory approach towards the

losing candidate Clinton made all the previous assumptions awfully wrong for a

prolonged “dooms day” scenario, in case of an “unexpected” win by Trump.

Thus,

its hope of “Trumponomics”; i.e. higher fiscal spending to the tune of $1 TLN

in next 10 years (?), big corporate & personal tax rate cuts, reduced

regulations which is propelling the US market. Eventually, as a result of

“Trumponomics”, US growth & inflation and employment may gather momentum

and subsequently, corporate earnings may be also getting some incremental

growth.

As

par some analysis, original tax & budget plan of Trump may have cost US

Federal debt by around $11.5 TLN over next 10 years; but after modification

done by his “main stream economists” team, it might cost US debt by around $5.3

TLN.

Now,

all will depend upon the actual “budget plan” and future “vision plan” by Trump

& his team after taking charge of Oval office on 20th Jan’17. In

reality, it may take significant longer time for necessary negotiations within

the US Congress, its ultimate passage and actual implementation; size of the

overall fiscal spending may also be reduced by the US Congress; otherwise it

will cause huge budget hole and US has to take more debt to fund its fiscal

deficit.

It’s

precisely the perception of more supply of US debts/TSY Bonds, which is

propelling the US bond yields & USD to a record high, apart from another

primary reason of USTSY bond sales by China & some private investors.

But,

ultimately the whole idea of “Trumponomics” may be a fantasy and may also cause

US economy towards a deflation; i.e. higher inflation & stagnant growth/GDP

instead of a simple “Trumpflation” (higher inflation & higher growth).

After

initial days of euphoria, now some election campaigning day rhetoric may be

also coming back in the form of harder trade policies, imposition of additional

import duty in order to encourage “Made in USA” theme and anti China stance,

which may also invite similar retaliatory action from other countries, which in

turn may cause a wave of “trade war” along with the current “currency war”.

Eventually,

higher import duties, if implemented may also cause higher cost of US

manufactured products and incremental higher inflation, much beyond Fed’s

projection of 2% and may run towards 5% level within a year or two, which in

turn may force Fed to go for much more rapid rate hikes than projected in its

dot plots and as par some estimates, USD may gain almost 15% in that scenario

from the present level.

It’s

also unusual to have a direct co-relation of US EQ market with USD and its

usually an inverse co-relation (a strong USD is usually negative for US stocks,

considering not only for US exports, but also for overseas US corporates, which

has to report their earnings in USD, but actual earnings are happening in local

devalued currency). Thus, a cross currency headwinds for US corporates may be

one of the biggest risks under “Trumponomics”, if implemented in its actual

rhetoric.

As

par some reports, all else being equal and 5% surge in USD may translates

around 3% dips in earnings for US corporates and 0.5% in US GDP. After

“Trumpism”, dollar index already gained by 5% (DXY). USD gained significantly

against almost every other major G-10 currencies as well, which may affect

Q4FY16 earnings for the US corporates and affect the sentiment of the market,

despite perception of future corporate tax cuts and incremental capex by the

Govt.

Valuation

wise, for the SPX-500, the current TTM PE of around 25.62 may also be quite

expensive and in a bubble zone against its average PE of around 16. Current TTM

PE may also be highest since 2008 economic crisis.

For

SPX-500: 2263.79 (Spot)

Q3FY16

TTM EPS: 88.36

FY15

EPS: 88.43

FY14

EPS: 105.32

FY13

EPS: 103.93

FY12

EPS: 91.08

FY11

EPS: 93.14

FY10

EPS: 85.31

Average

EPS for last 5 years: 95.76 (FY10-FY-14)

Actual

growth for FY15 EPS: -16% (YOY)

FY15

EPS growth: -7.65% (from average of 95.76)

Mean

growth in FY15 EPS: (-) 11.82%

Against

this backdrop:

Projected

FY16 EPS: 117.56 (i.e. more than 26% growth from FY15)

Projected

FY17 EPS: 133.96 (i.e. around 12% growth from projected FY16)

Projected

FY18 EPS: 147.97 (i.e. around 10% growth from projected FY17)

Projected

FY16 EPS at around 118 may also be looking tough even on the back of buy back

of shares by various US corporates (courtesy Fed’s easy money policy), recent bounce

in oil & improvement in EPS of energy related shares and Q2FY16 softness in

USD.

But

the projected EPS growth for FY17-18 may be even tougher, considering recent

& future strength in USD, saturation in oil and base effect for the buyback

of shares. The projected US earnings growth of around 10-12% may be also looked

quite stretched on the back of tepid global growth, stress in China, various

geo-political risks in EU and trade barriers rhetoric by Trump, despite

proposed corporate tax cuts and huge Govt capex.

For

an economy, where GDP is growing around 3%, it may also be very tough for the

average US earnings (EBITDA) & EPS to grow above 12-15%; i.e. 4-5 times of

GDP growth. Top line (operating revenue) of US corporates may not be growing as

expected and the beat in EPS may be coming on the back of buy backs & other

non-operating income and tax benefits.

One

of the tailwinds for the US economy may be lack of any wage inflation and tepid

earnings growth. Although, the headline job numbers and employment data may be

looking great at this point of time, it also came on the back of lower

participation rate (which inflates the employment % rate) and lack of quality

jobs.

A

stronger USD and a hawkish Fed (higher dot plots) may ensure overall

incremental higher interest (finance cost) for the US economy in the coming

years and both US household debts (mortgage/auto/credit card/student loans) as

well as corporate debts/SME loans may be under immense pressure.

Having

said that, Fed’s actual action till 2018 may depend largely on trajectory of

“Trumponomics” & actual size & implementation time of the proposed

fiscal spending plan and depending upon that Fed may either hike 0.50-0.75%

both in 2017-18. Trump’s huge fiscal spending plan may also be largely

dependent on the “easy money” policy of ECB & BOJ; otherwise who will fund

the “Trumponomics” ?

But,

going by the present trend of nationalistic politics and trade protectionism,

especially after “Brexit” & “Trumpism”, EU politicians & policy makers

may be forced to abandon the “easy money policy” (QQE) gradually and may take

the path of higher fiscal spending (structural stimulus) for the benefit of

“real street” instead of relying too much on the monetary stimulus for the

benefit of “wall street”.

ECB,

BOJ and also PBOC & other G-10 countries may take less dovish monetary

stance and may also move towards gradual normalization in the coming months in

order to keep the policy parity (bond & interest rate differential) and USD

FX rate with their local currency at an equilibrium level, considering both

external & internal economics issues.

SPX

SPX

DJ

DJ

No comments:

Post a Comment