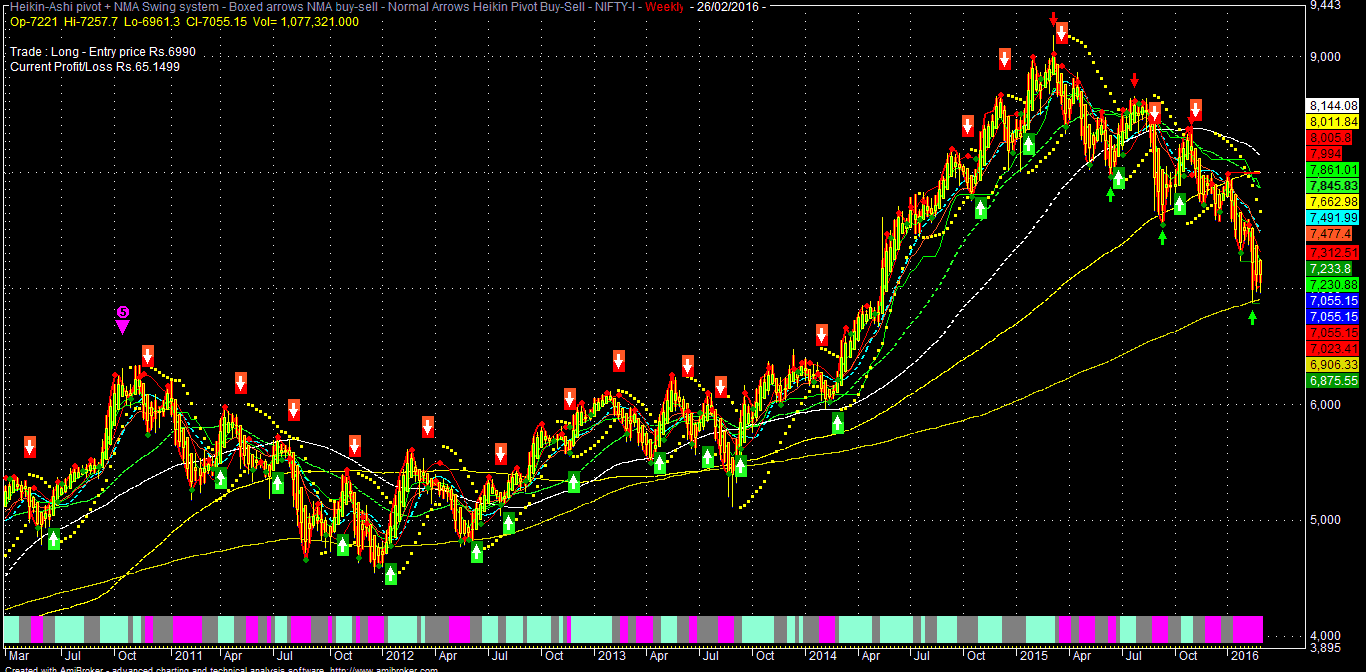

NF need to sustain over 7215-7295 zone for any rally towards 7560-7595;

Otherwise, it may be weak and below 7015-6960 zone,

may again fall towards 6875-6775 area.

7-PC based consumption boost may be not sacrosanct

as previously expected overall economic recovery magic !!

may again fall towards 6875-6775 area.

7-PC based consumption boost may be not sacrosanct

as previously expected overall economic recovery magic !!

Trading Levels: Nifty Fut (Mar)

SGX-NF: 7040 (LTP)

NSE-NF: 7061 (LTP)

| SL (+/-) 10 POINTS | FROM SLR | |||||||

| For | Intraday Swing | Trader | ||||||

| T1 | T2 | T3 | T4 | T5 | SLR | |||

| Strong > | 7170 | 7215-260* | 7295-350 | 7375-435* | 7475-490 | 7560-595* | <7150 | |

| Weak < | 7150 | 7115-090* | 7055-015 | 6990-940* | 6905-875 | 6850-775* | >7170 | |

| FOR | Conservative | Positional | Trader | |||||

| T1 | T2 | T3 | T4 | T5 | SLR | |||

| Strong > | 7170 | 7295* | 7375 | 7435* | 7560 | 7640-750* | <7150 | |

| Weak < | 7150 | 7090* | 7015 | 6940* | 6875 | 6775-570* | >7170 | |

After no G-20 co-ordinated CB action on Saturday, global markets are trading somewhat lower as various statements by G-20 leaders apparently showed that they are not so much "concerned" about the current global market turmoil and they will continue to keep "close watch" on the FX world/market.

Back to home, as par our PM, today may be an "exam day" for him/his Govt, being the budget day.

Some of the important highlights, market will watch for this budget:

FY-16 actual fiscal deficit figure, which is likely to be between 3.7-3.9% of GDP.

FY:17-18-19 FRBM road map, which is expected between 3.5-3% of GDP. Too much deviation from the previously announced FRBM targets, may attract rating agencies action/downgrade.

FY-17 gross borrowing targets & capex for the Govt. A strong dose of infra spending is expected to compensate for the poor private sector investment, even at the cost of some fiscal consolidation.

7-PC/OROP implementation road map, which is expected to stagger over three years. Some measure to boost consumption through direct tax concessions, like SD increased from Rs.2 lakhs to Rs.3 lakhs and few more sops are expected.

1% cut in corporate tax as par plan of 25 to 20% within 2019 with exemptions withdrawal (revenue neutral for Govt, but overall some net higher tax outgo for some corporates also).

Hike in service tax from present 14.5% to around 18% as par GST road map (negative for overall economy as it may result in somehow higher inflation, with virtually no hope for GST implementation even by FY-17; in the back drop of current political scenario and forthcoming state elections, there is little hope for any consensus regarding passage of important bills like GST in the RS).

PSBS recapitalization road map apart from the present "Indradhanush".

Higher lock in period for LTCG from present 1 to 3 year is expected; but in the present scenario of weak market sentiment, Govt may not choose to tinker with these.

Govt is expected to abolish DDT & STT; but taking into the revenue angle, Govt may not oblige for any STT cut.

Some Budgetary steps to boost rural economy & social sector spending aiming for the coming five state elections (in which BJP is expected to loose in all the states !!).

FY-17 divestment plan, strategic sales of Govt assets (non-core PSUS to fund PSBS)

Road map for "Start Up" & "Make In India" funding.

Road map for subsidy rationalization.

After no such economic recovery as highly expected in the last two years, market is now keeping hope on 7-PC based demand & consumption growth. But, given the staggered nature of the implementation and the current subdued market condition and tepid confidence of the Indian consumers, no big-bang consumption may actually happen apart from some low ticket ones.

Its not sacrosanct that people will start into buying spree as soon as they got the 7-PC arrears; instead they may go into savings mode for their future generations.

Analytical Charts:

No comments:

Post a Comment