Market

Wrap: 01/11/2016 (16:30)

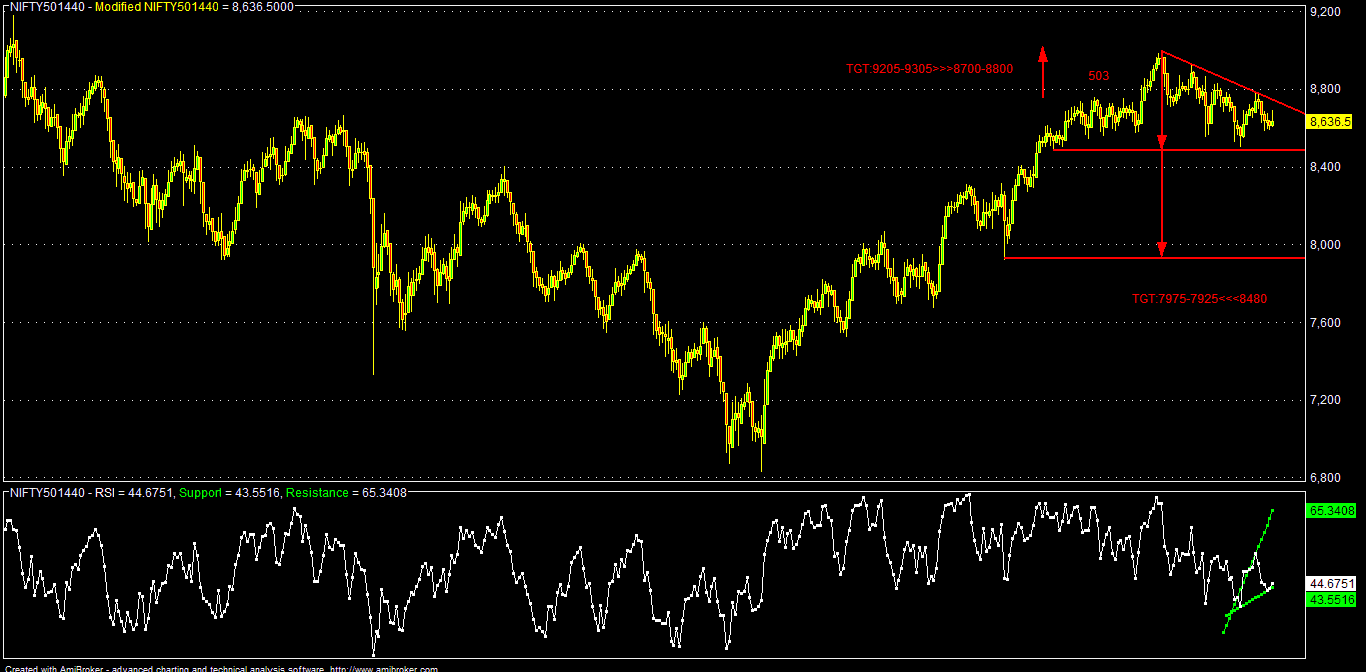

Nifty

Fut (Nov), today closed around 8650, almost flat after an opening session low

of 8633 and day high of 8705 following tepid global & no meaningful

domestic cues.

Technically, for

tomorrow (02/11/2016), NF has to sustain over 8670-8705* area for further rally

towards 8730/8760*-8790/8815-8870/8900 zone in the immediate to short term.

On the other side,

sustaining below 8615-8580* area, NF may further fall towards 8540*-8500-8465

& 8405 zone in the immediate to short term.

As

Indian market was celebrating "Diwali" in the weekend, some global

headwinds resurfaced:

FBI decided to investigate another series

of Clinton e-mails. Apart from immediate impact on Clinton presidency prospect,

the ongoing investigation, if not concluded shortly, then it may also cast some

doubt about Clinton's ability to take charge of the President's office for

compliance reasons, even if she wins. After this FBI news came to light,

pre-poll difference between Clinton & Trump narrows quite significantly.

There was some market buzz that BOE Gov Carney may resign early around mid- 2018 for some controversy over the Brexit stand; but later he clarified that he will stay one more year (June’2019) in order to help UK for a smooth exit transitions or “divorce” from EU.

Oil was under pressure as OPEC & Non-OPEC meeting in Vienna actually failed and weekend data also showed that more taps are coming online. Some analysts are predicting for $40 oil, if Nov OPEC meet fails to do any production cut or even freeze.

Today’s

morning global cue was mixed after BOJ holds the “Bazooka”, but delayed the

projected time line for achieving its target of 2% inflation, which may also show

that decades of QQE has not worked as expected. The overall BOJ stance may be

also indicating their desire to steepen the JGB yield curve.

Global

sentiment improved further today in early Asian session, after Chinese PMI data

came above market expectation, which may an indication that “hard landing” is

not immediate for China. But, continuous devaluation of Yuan, record liquidity

injection by PBOC and start of trading in CD may make the market cautious too.

Overall

sentiment of the “risk trade” may be quite subdued for this eventful week

(BOJ/BOE/Fed/US Job Data), till Nov-11, until US election result will come.

Among

all these global concerns, Indian market was also under some pressure as firing

& shelling is continuous on the LOC (Pak) and it’s like a “virtual mini war”

there in the border. But, mixed macro & better monthly auto sales data may

bring some cheers for the market.

India’s

Fiscal Deficit almost reached 84% of the FY-17 BE and that’s may be a cause of

concern (higher 7-CPC/OROP pay out, incremental defence expenditure & infra

capex and lower proceeds from telecom spectrum auction). Looking ahead, Govt’s

capex may go slow, especially if targeted disinvestment is not met. As private

capex is not visible due to various reasons, Indian economy is now greatly

dependent on Govt capex.

But

better core sector output & PMI data today may have complemented the

alarming fiscal deficit figure.

In

the last hour of trading today, some survey was released in EU, which predicted

Italy may be the next country after UK to choose another “divorce” from EU.

Thus, the geo-political risk in EU may be turning serious (German & French

election, Scottish referendum, Grexit & EU/Italian banking crisis and NPL)

and “risk on” sentiment again dipped globally as well as for the domestic

market.

Indian

market sentiment was also hurt today again at the fag end of the market after

Mistry throws another “bomb” contesting the Tata Sons about the Docomo &

some other issues. Although, Tata group is maintaining that they will go by the

planned deleveraging & restructuring way for various group companies,

market may be still not impressed enough as various potential high level exits

may cause some serious management jitters in the days ahead.

As

the “war of words” between Tata Sons & Mistry getting louder and the matter

even goes to the PMO, market sentiment is still jittery about the overall

incident, which may have also dented “India’s corporate dignity” globally.

SGX-NF

No comments:

Post a Comment