Market

Wrap: 01/02/2017 (19:00)

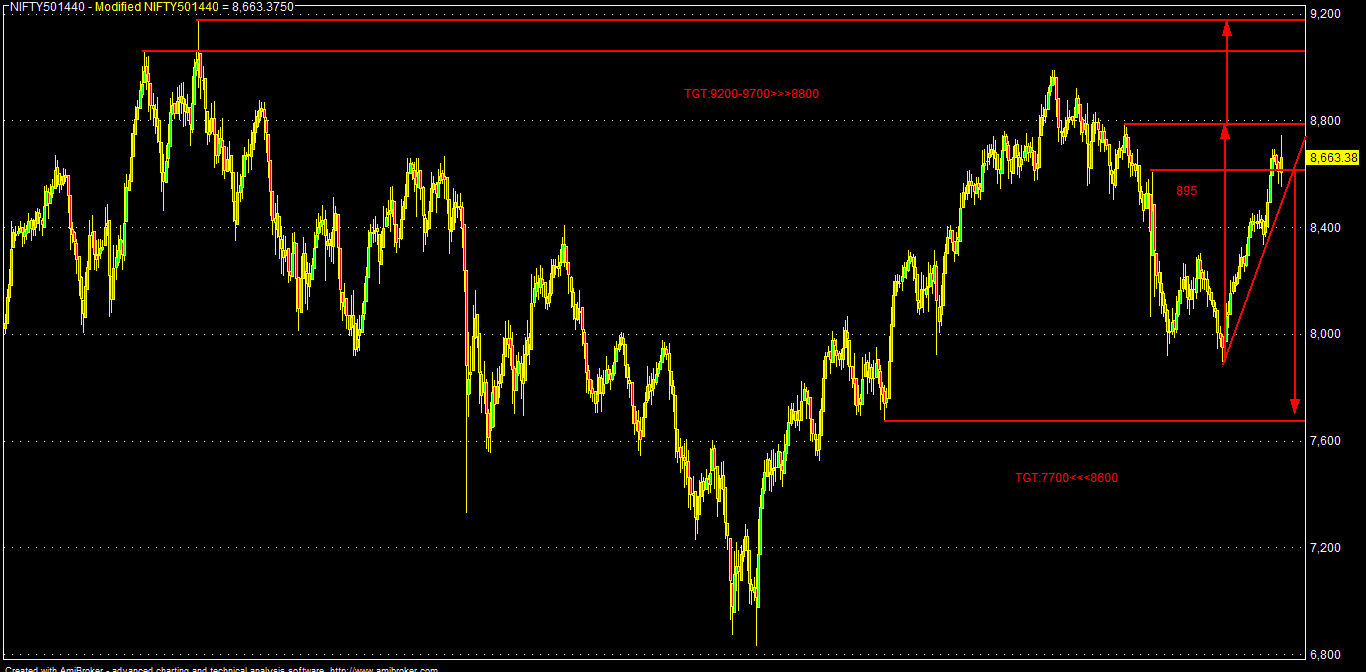

Looking at the chart, Nifty Fut (Feb @8736)

has to sustain over 8765-8800 area for further rally towards 8855-8895 & 8935-8995

zone in the short term (under bullish case scenario).

On the other side, sustaining below 8725-8690

zone, NF may fall towards 8625-8545 & 8455-8365 area in the near term

(under bear case scenario).

In the absence of any negative surprise

(capital market tax reform & FPIS taxation issues) for which the market was

very concerned, today’s budget day rally may be more of a relief rally primarily

driven by huge FNO short covering amid some cut in income taxes for the low

income bracket (Aam Admi) and thrust on infra & rural spending and fiscal

prudence. Going forward, fine print of the budget and its proper implementation

may be the key.

Nifty

Fut (Feb) today closed around 8736 (+152 points) after making a session low of

8555 and closing hours high of 8747.45 after the presentation of FY-18 budget.

Today’s budget day rally is the biggest in the history of last twelve years

(since 2005) and more over, NF rallied by almost 192 points from today’s low of

8555, respecting the 10-DEMA after FM announced FY-18 projected fiscal deficit as

3.2% of GDP against market estimates of 3.3-3.5% and reduction of income tax

from 10% to 5% for the lower income category (2.5-5 lakh). As FM finished the

budget speech, market realized that there is no “capital market tax reform” for

the “development of the nation” as previously feared by the market participants

(i.e. rejig of LTCGT definitions etc & FPIS taxation issues), Nifty rallied

from around the day low aided by huge short covering.

Bank

counters also rallied significantly by around 2.70%, outperforming the Nifty as

there was a budget proposal for increased income tax relief for bad loan

provisions (from 7.5 to 8.5%). Also the Govt’s plan to infuse additional

Rs.10000 cr for recapitalization for the ailing PSBS in FY-18; but analysts are

not sure, if this amount is additional capital infusing plan over the current “Indradhanush”

plan or not (Rs.75000 cr per year from 2015 to 2019); FY-18 recapitalization

plan of Rs.10000 cr may be below market estimates, although Govt has assured no

deficiency in funding of PSBS, if there is a real need. Also, projected FY-18

Govt borrowing came at Rs.3.48 tln, which is below FY-17 revised estimate of Rs.4.1

tln may be good for the banks.

Thus,

incrementally higher Govt capex, balanced approach in fiscal prudence and no

negative surprise on the capital market tax reform issues in the budget today

may have ignited the rally. The market sentiment was further boosted by better

than expected Mfg PMI (Markit) which came above boom/bust line of 50 for Jan’17

after last month’s dip (PMI: 50.4; estimate: 49.7; prior: 49.6) and upbeat

monthly auto sales figure from Maruti for Jan’17, despite demonetization blues.

Today’s

budget proposal to abolish FIPB for FDI approval may have also boosted the

market sentiment for the theme of ease of doing business in India (entry &

exit); but Govt will probably put an alternative mechanism (regulation) for it

in the days ahead.

Granting

infra status to affordable housing is also positive for some of the real estate

companies and banks & NBFC; although it is in expected line, some of the

companies (DLF/DHFL/HDFC Duo/Gruh Finance/IRB Infra) may benefit; also

reduction in import duty for LNG is positive for Petronet and rural thrust may

be also positive for FMCG. Less than expected ED on cigarettes and fresh duty

on tobacco products may be good for ITC. Having said that, all the stocks need

to be checked technically, if there is any further scope for rally in the near

term or not.

As the market/analysts/rating agencies will

further analyze the fine print of the FY-18 budget and actual figure for FY-17

in the coming days, the near term trajectory of the Indian market may also depend

on the Q3FY17 & subsequent Q4FY17 earnings recovery cycle, which is

mixed/tepid so far, further evidence/data of economic disruptions for the

demonetization, pace of remonetization, uncertainty about implementation of GST

in FY-18 & any initial disruption thereof and overall various global

headwinds including Trump tantrum and trajectory of global commodity prices,

specially crude oil.

As

par some estimates, today’s income tax relief to the lower income group may

save around Rs.12000/- par tax payer, which may help to boost consumption

(demand) for the economy, bracing under demonetization & “war on black

money”. But, in reality, a gross income up to Rs.5 lakh PA may not invite any

actual payment of income taxes, if one planned appropriately thanks to various

available exemptions. Moreover, a savings of 12000/- PA or 1000/- PM for

limited sets of income tax payers may be of little help to revive the great

Indian consumption story, which was traditionally too much dependent of the “unaccounted

black money”; at least 30% of that high value consumption may be affected as

the “war on black money” continues. Rebuilding & redistribution of that “lost

wealth” may take several years, despite Govt’s best effort to recapitalize the

same at the earliest.

Only

some limited tax relief may not be sufficient to sustain the present market

rally; it has to be backed by revival in growth & earnings and for that

revival of private capex is also required. Incremental Govt capex may also

result in higher Govt debt/GDP ratio, which may be one of the deterrent of

India’s rating upgrade, which is just one notch above international junk grade.

Although,

market have rallied on various positive budgetary proposals, implementation of

the same is key and can correct also very fast, if reality does not catch up

with the hopes (projections).

Earnings

need to be also catching up with the rally; at 8700-8800 level, Nifty TTM PE

may be around 23.2-23.46 (based on actual Q2FY17 TTM EPS of around 375) and

even if, FY-17 final EPS come around 415, projected FY-17 PE may be around 21,

which is historically on the higher side.

As time & price action is the

ultimate, irrespective of any narratives, keep watch on 8765-8800 zone in NF;

only a consecutive closing above that may invite further rally towards

9000-9200 & even 9700 in FY-18; otherwise it will come down towards 8455-7900

& 7700 in the coming months, if sustained below 8600.

SGX-NF

No comments:

Post a Comment