Market Wrap: 05/04/2017

(19:00)

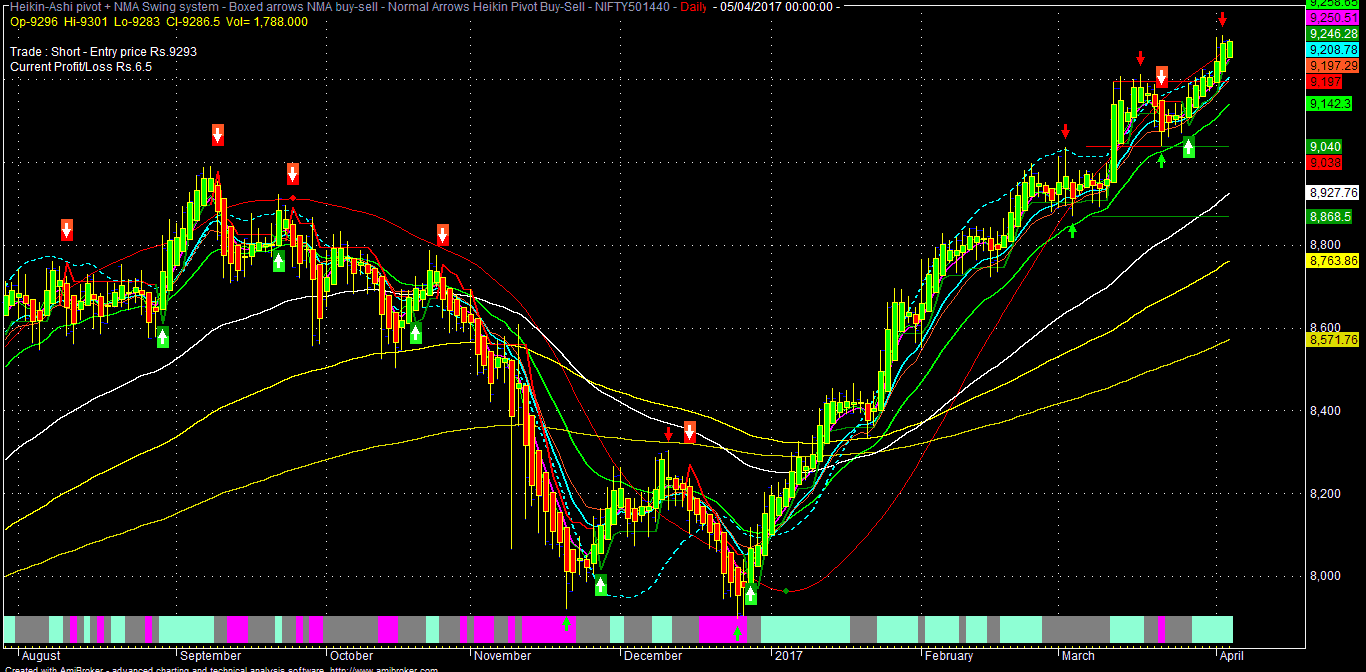

NSE-NF (April): 9283

(+19 points; +0.21%)

NSE-BNF (April): 21665

(+88 points; +0.41%)

For 06/04/2017:

Key support for NF: 9245-9195

Key resistance for NF: 9325-9375

Key support for BNF: 21650-21450

Key resistance for BNF:

21775-21875

Time & Price action suggests that,

Nifty Fut (Apr) has to sustain over 9325 area for further rally towards 9375-9425

& 9465-9505 by tomorrow / in the short term (under bullish case scenario).

On the other side, sustaining below 9305

area, NF may fall towards 9245-9195 & 9140-9090 area by tomorrow / in the

short term (under bear case scenario).

Similarly, BNF has to sustain over 21775

area for further rally towards 21875-21950 & 22050-22150 area by tomorrow /

in the near term (under bullish case scenario).

On the other side, sustaining below

21725 area, BNF may fall towards 21650-21525 & 21425-21300 zone by tomorrow

/ in the near term (under bear case scenario).

Nifty

Fut (Apr) today closed around 9283 after a range bound day of trading, in which

it made an opening session low of 9248 and day high of 9295. Nifty was

supported today by RIL, LT & Maruti, but dragged by HDFC, ITC & Infy.

PSBS were also in the limelight today amid merger of different SBI groups &

UP farm loan waiver.

The

huge farm loan waiver of Rs.36353 cr by UP Govt announced yesterday as par

their election promise may be good for the PSBS in the sense that they will be

reimbursed of the waiver amount by the Govt itself; but it may also bad for the

overall credit & fiscal discipline of the banking system as also for the

combined state & centre fiscal deficits. Such farm loan waiver is not new

and it happens in 2008 also under UPA Govt also and this is becoming a bad

precedent. All the other states may also adopt such political populism at the

cost of the exchequer during poll times and borrowers (farmers) may also wait for

another election for such “golden opportunity”. Even honest borrower (farmer),

who paid his loan may be feel cheated after such Govt sponsored farm loan

waiver. At the same time, other types of distressed borrowers be it retail or

MSME or corporate may also demand for such waiver as the policy should be the

same for all types of borrowers and thus the overall credit discipline of the

banks & MFI(s) may come under some pressure in the days ahead. Govt/RBI

need to formulate some practical “waive off” or “hair cut” policies for the NPA

mess of the Indian Banking system and some reform may also be required to

address the root cause of the stressed assets, be it of farmers or of corporates.

All eyes may be on the RBI tomorrow for any steps towards speedy resolution of

the NPA saga of the Indian Banking system.

Market

may also watch RBI’s statement or commentary in addition of any step towards

liquidity adjustment of excess DeMo (special parking facility without accruing

any incremental SLR). As there is absolutely no hope for a rate action (cut)

tomorrow, market may give emphasize on RBI’s statement (hawkish or dovish).

Considering all the global factors such as improving US economic data, a hawkish

Fed preparing for another 2-3 rate hike in 2017-18, a sticky domestic core

inflation hovering around 5%, a high probability of a deficient monsoon in 2017,

RBI may adopt a hawkish or rather owlish stance instead of a dovish tone

tomorrow.

An

economy growing at 7-8% need not require any further incremental rate cuts from

the central bank also and being an inflation hawk, Patel may also sound quite

hawkish considering there is very limited scope of further rate cut

transmissions by the banks unless small savings rate is reduced drastically,

which may be again a very tough political decision for the Govt. Also, Govt/RBI

may not want to reduce repo rate further drastically as it may also affect the Indian

bond yields adversely, which in turn may also affect the FPI(s) flow (hot money

by yield hungry investors).

Globally,

also no major central banks are now talking about rate cuts as Fed is on the

multiple rate hikes path and thus RBI also can’t afford to be divergent in the

months ahead; there may be no probability of any further rate cuts in FY-18. RBI

has already shifted to neutral from previous accommodative mode and thus, Patel

may give emphasize on the inflation trajectory to ensure “not too much hot”

Indian economy and may also take cautious stance for any DeMo spillover effect

& GST implementation and its effect on CPI before official IMD forecast

about Indian monsoon trajectory.

Globally,

USD/US bond yields jumped after blockbuster US ADP payroll data for March,

which flashed as 263k against estimate of 187k (prior: 245k-revised). SPX-500

also trading higher at around 2363 on the improving outlook of US economy; all

eyes may be now on the ISM Non-Mfg PMI & FOMC minutes to gauge Fed’s appetite

for more rate hikes in 2017 and any plan of balance sheet size reduction.

Technically, SPX-500 need to sustain

over 2375-2405 level for further rally towards 2430-2465 & 2500-2550 area;

otherwise it may come down again and sustaining below 2335-2325 area, may further

fall towards 2305-2275 & 2235-2210 zone in the short to mid-term.

For

SPX-500, at recent high of around 2400 and TTM EPS (FY-16) at around 119, TTM

PE may be around 20.17, which is quite stretched, considering its median

average PE of 15 for the last few years.

Valuation

metrics for SPX-500:

Actual

FY-16 EPS: 119.15; Average PE: 18

Median

Valuation: 2145 (FY-16 TTM)

Projected

FY-17 EPS: 126.90 (As par current & implied run rate); Projected PE: 18

Projected

Median Valuation: 2284 (FY-17 FWD)

Projected

FY-18 EPS: 136.45 (As par current & implied run rate); Projected PE: 18

Projected

Median Valuation: 2456 (FY-18 FWD)

Actual

Run rate of SPX-500 EPS:

|

SPX-500

|

Dec'16

|

Dec'15

|

Dec'14

|

Dec'13

|

Dec'12

|

FY-12-16

|

FY-15-16

|

AVG

|

AVGR

|

SGR

|

PROJ(%)

|

FY-17

|

FY-18

|

|

EPS

|

119.15

|

118.60

|

118.96

|

111.36

|

105.25

|

13.21

|

0.46

|

113.54

|

4.94

|

3.12

|

2.96

|

122.67

|

126.30

|

|

VALUE

|

2233.50

|

2035.75

|

2051.50

|

1846.00

|

1408.00

|

58.63

|

9.71

|

1835.31

|

21.70

|

10.95

|

14.25

|

2551.88

|

2915.64

|

|

ACTUAL PE

|

18.75

|

17.16

|

17.25

|

16.58

|

13.38

|

40.12

|

9.21

|

16.09

|

16.49

|

8.02

|

10.94

|

20.80

|

23.07

|

|

AVG PE

|

18

|

18

|

|

|

|

|

|

|

|

|

|

18

|

18

|

|

FAIR VALUATION

|

2145

|

2135

|

|

|

|

|

|

|

|

|

|

2208

|

2273

|

|

EPS CAGR(%)

|

0.46

|

-0.30

|

6.82

|

5.81

|

|

|

|

|

|

|

|

|

|

|

SPX-500

|

Dec'11

|

Dec'10

|

Dec'09

|

Dec'08

|

Dec'07

|

FY-12-16

|

FY-15-16

|

AVG

|

AVGR

|

SGR

|

PROJ(%)

|

FY-12

|

FY-13

|

|

EPS

|

98.97

|

87.10

|

62.02

|

73.74

|

87.48

|

13.13

|

13.63

|

77.59

|

27.56

|

4.88

|

12.34

|

111.18

|

124.90

|

As

par actual run rate for the last few years, projected EPS growth may be around

6.5% for FY-17 & 7.5% for FY-18, considering share buyback, muted earnings

growth in energy related companies as upside for oil may be limited in FY-17.

|

SPX-500

|

EPS

|

|

ACTUAL FY-16

|

119.15

|

|

PROJ FY-17@6.5% CAGR

|

126.9

|

|

PROJ FY-18@7.5% CAGR

|

136.45

|

|

Valuation Metrics

|

FY-16

|

FY-17E

|

FY-18E

|

|

TTM EPS

|

119.15

|

126.90

|

136.45

|

|

MEDIAN PE

|

18

|

18

|

18

|

|

MEDIAN FAIR VALUE

|

2144.70

|

2284.20

|

2456.10

|

Analyst’s

EPS projection (consensus):

|

ANALYST PROJECTION

|

FY-17

|

FY18

|

|

EPS

|

131.13

|

146.61

|

|

PROJ CAGR(%)

|

10.05

|

11.81

|

Ideal

Median PE of 15 may also be expensive, considering, projected growth of average

EPS of around 5-7%; actual run rate 3%; EPS growth between FY-15 & 16 is

mere 0.46%; may be market is too much optimistic about “Trumponomics” or reflation

(Trumpflation) trade

As

par JPM, base case EPS for SPX-500 may be around 128 (FY-17) and depending upon

various scenarios of tax reform (cut), the projected EPS may be around 133-137

(when such tax reform will be implemented).

But,

strength of USD may also be another concern for US corporate earnings, which is

so far dependent largely on the energy prices (oil) in recent times. Another

point is that despite record consumer sentiment, consumer spending (retail

sales) may be still tepid and March auto sales were also below estimate. Thus,

some analysts are also very concerned about such divergence in soft & hard

data of US economy and something may be wrong.

SGX-NF

BNF

SPX-500

No comments:

Post a Comment