Market Wrap: 14/06/2017

(17:00)

NSE-NF (June): 9638

(+23; +0.24%) (TTM PE: 24.35; Near 2 SD of 25; TTM EPS: 395; NS-9618)

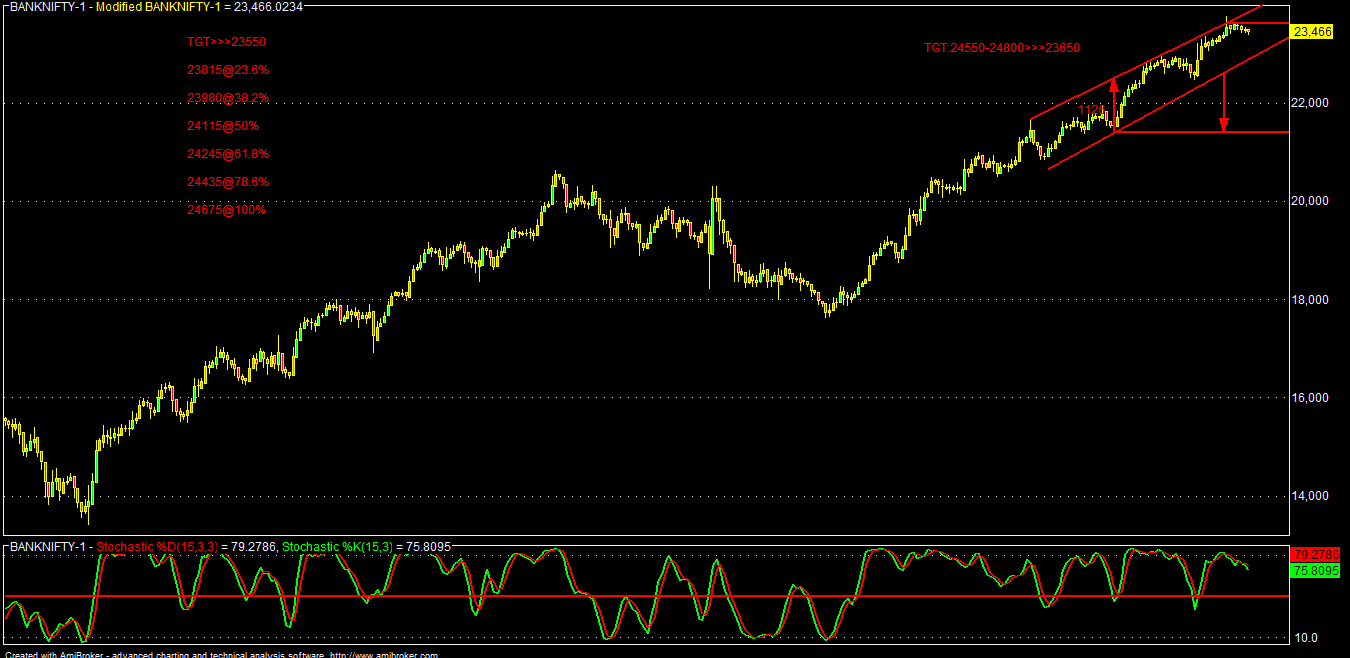

NSE-BNF (June): 23492

(+43; +0.18%) (TTM PE: 29.56; Near 3 SD of 30; TTM EPS: 795; BNS-23499)

For 15/06/2017:

Key support for NF: 9580-9525

Key resistance for NF:

9675-9715

Key support for BNF:

23350-23200

Key resistance for

BNF: 23650-23750

Time & Price action suggests that,

Nifty Fut (May) has to sustain over 9675 area for further rally towards 9715-9770

& 9825-9865 in the short term (under bullish case scenario).

On flip side, sustaining below 9655

area, NF may fall towards 9580-9525 & 9490-9395 area in the short term

(under bear case scenario).

Similarly, BNF has to sustain over

23650 area for further rally towards 23750-23875 & 24000-24100 area in the

near term (under bullish case scenario).

On the flip side, sustaining below

23600 area, BNF may fall towards 23350-23200 & 23050-22950 area in the near

term (under bear case scenario).

Nifty

Fut (June) today closed around 9638, almost 23 points up after trading most of

the days in sideways; it made a late day high of 9647 and opening session low

of 9598 and made some recovery in the last hour supported by sharp pull back of

midcap index and soma PSBS amid consolidation buzz of the sector.

Indian market today opened almost flat amid mixed global cues.

Overnight US market, DJ-30 closed in positive (+0.44%) at another record high

following better than expected core PPI and some bounce back in tech shares.

Also, US AG Session’s senate testimony was positive for the market as he

declined to say anything about his or Trump’s alleged link with Russia citing

“executive privilege”. But, still we may see more such US political jitters

regarding Trump-Russia election link as US senate may be very serious to

investigate the actual truth behind it.

Globally, today all focus will be on the deluge of US economic

data and Fed, which is poised to hike 0.25%, if it springs no nasty surprise.

But more than rate cut, market may emphasize more on Fed’s statement, its

future guidance/dot-plots, economic projection etc for another hike in Dec’17

or not as Sep is now being virtually ruled out. So, it may be a dovish hike

today by Fed, but Yellen may indicate gradual B/S tapering from Sep/Dec’17

onwards in lieu of further rate hike in 2017 amid soft US economic data &

poor visibility of “Trumponomics”. A taper tantrum by Fed may not be good for

the risk assets as it will be the indication of real normalization (Fed still

reinvests maturity proceeds from the QE bonds in the USTSY & MSBS and

selling of those QE bonds may hamper market liquidity seriously)

In the morning today, China flashed an upbeat IIP & Retail

data, but China market was trading in negative as better Chinese economic data

may not be good for stimulus hungry market; PBOC may continue to keep its

present neutral monetary policy except some targeted MLF. Also, fixed

investment data from China came below expectation, which may be also not good

for the overall Chinese economy. But, later upbeat GDP projection by IMF has

supported the China/Asian market sentiment along with India also.

For India, WPI came today at 2.17% for May (YOY) against

estimate of 3.11% (prior: 3.85%), which may have also supported the market

sentiment as it will keep more pressure on the RBI to cut in August. Also,

invocation of IBC act by RBI may have supported some private banks (ICICI)

today, although in the short term, banks may have to take huge haircuts. At the

same time, IBC may itself face various legal hurdles, times and challenges,

which may also raise serious questions of the actual resolution itself.

PSBS were in the limelight after Govt identifies some big PSU

Banks (BOB, Corp Bank), having sufficient B/S strength for consolidation with

other small PSBS (like Dena bank). RIL was in the limelight after TRAI data

shows blockbuster customer acquisitions for April with leadership position in

WL BB.

Overall, today domestic market was choppy amid some concern of

GST disruptions as Govt is committed for the 1st July launch with

barely 17 days in hand and the nation/business community may not be yet fully

yet prepared for the implementation of the same. The present GST format may be

too complex and compliance cost may also be significant. The main purpose of

this GST launch in a hurry without considering the stakeholders lack of

preparation may be Govt’s larger aim to track all the business transactions and

stop the revenue leakage loopholes thereby (war against unaccounted money). The

GST may be simplified by next few years after initial feedback. But, market may

be apprehending some adverse effect on the corporate earnings in Q1& Q2FY18

because of GST disruptions.

Today Nifty was dragged by Yes Bank, ITC, HDFC, ACC, Tata Steel

and some Pharma shares (Cipla, Auro Pharma).

Elsewhere, Oil was under pressure after surprised inventory

buildup in API data yesterday; today official EIA data will be in focus.

Recently, we have seen major divergence between API & EIA oil inventories

data. Also, a report from IEA highlighting increased oil production from NOPEC

countries and resumption of Nigeria & Libya oil field may be again causing

some pressure on oil for the concern of increasing supply glut.

Meanwhile,

USD Plunged After Subdued Core CPI & Terrible Retail Sales Data Ahead Of

Fed.

US

just flashed the data for May as:

Core

CPI (MOM): 0.1% (EST: 0.2%; PRIOR: 0.1%)

Core

CPI (YOY): 1.7% (EST: 1.9%; PRIOR: 1.9%)

CPI

(MOM): -0.1% (EST: 0.1%; PRIOR: 0.2%)

CPI

(YOY): 1.9% (EST: 2%; PRIOR: 2.2%)

Core

Retail Sales (MOM): -0.3% (EST: 0.2%; PRIOR: 0.4%)

Retail

Sales (MOM): -0.3% (EST: 0.1%; PRIOR: 0.4%)

In

one word, overall data may be quite terrible and although Fed may hike today,

it may be a “dovish hike” and probability for a Sep hike is now plummeted to

18% vs 24% and for Dec, FFR is now showing 46% vs 53% before the data. Market

may be now discounting no Fed hike in Sep as also in Dec’17. Fed may shift to

neutral stance in the months ahead with some hints of gradual tapering of its

huge B/S.

After

CPI & retail sales data, USDJPY plunged to 109.30 level and EURUSD jumped

to 1.1278 zone. Gold also rallied to almost 1280 level.

Technically, USDJPY

(109.25) need to stay over 109.15 now; otherwise it may fall towards

108.15-107.20 & 106.15 before or after Fed depending upon Yellen’s script.

SGX-NF

BNF

USDJPY

Article Courtesy: frontiza.com

For Advisory Support:

https://t.me/MarketLive_free

No comments:

Post a Comment