Market Wrap: 02/01/2018 (17:00)

NSE-NF (Jan):10472 (-27; -0.26%)

(TTM PE: 26.71; Abv 2-SD of 25; TTM Q1FY18 EPS: 391;

NS: 10442; Avg PE: 20; Proj FY-18 EPS: 418; Proj Fair Value: 8360)

NSE-BNF (Jan):25393 (-54; -0.22%)

(TTM PE: 29.22; Near 3-SD of 30; TTM Q1FY18 EPS:

867; BNS: 25338; Avg PE: 20; Proj FY-18 EPS: 961; Proj Fair Value: 19220)

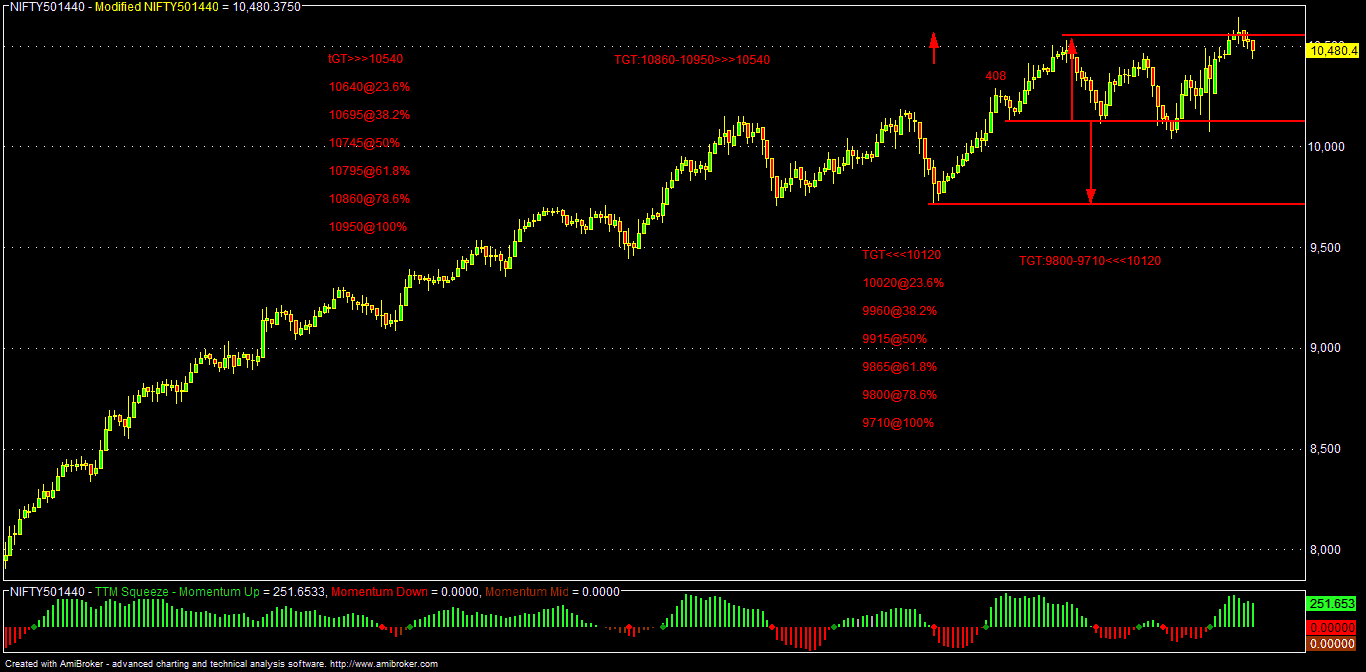

For 03/01/2018: Jan-Fut

Key support for NF: 10460/10415-10360/10325

Key resistance for NF: 10505/10575-10610/10650

Key support for BNF: 25200/24950-24800/24500

Key resistance for BNF:

25650/25775-25875/26050

Trading Idea (Positional):

Technically, Nifty Fut-Jan (NF) has to sustain over 10575 area for further

rally towards 10610/10650-10695 & 10745-10795 zone in the short term (under

bullish case scenario).

On the flip side, sustaining below 10555-10505 area, NF may fall towards

10460/10415-10360/10325 & 10300/10285-10240 zone in the short term (under

bear case scenario).

Technically, Bank Nifty-Fut (BNF) has to sustain over 25775 area for further

rally towards 25875- 26050 & 26200-26325 zone in the near term (under

bullish case scenario).

On the flip side, sustaining below 25725-25650 area, BNF may fall towards

25350/25200-24950 & 24800-24500 area in the near term (under bear case

scenario).

Indian market (Nifty Fut-Jan/India-50) today (2nd Jan) closed around 10472, slips by almost 27 points

(-0.26%) and off the opening high of 10524 on fiscal & LTCGT (long term

capital gain tax) worries amid holiday thinned subdued Global/EU cues (higher EUR); it made a session low of 10436, but recovered in late trade to close

almost flat; Asian cues were stable on upbeat China MFG PMI data and reports

that new property tax will not be imposed until 2020.

Market is also concerned about Q3FY18 earnings to

be released next week onwards and higher oil; but an upbeat MFG PMI data for

Dec released yesterday at 51.5 vs est 50.6; prior: 50.8 and core sector output

data (Nov) at 6.8% vs prior 4.7% may have cushioned the impact of macro worries

and market basically consolidated form 2017 closing of 10557 to 10436 (-1.15%)

on DII/MF year-end portfolio rebalancing (some profit booking after an

impressive 2017 gain-one year as LTCG) amid holiday thinned market.

Also, some encouraging auto sales figures may have

helped the market to some extent. Apart from fiscal & LTCGT worries, market

may be also concerned about ultimate fate of corporate NPA/NPL resolution with

so much stressed assets are on the block with various legal challenges, huge

hair –cuts through NCLT/IBC process and ongoing political controversies thereof

ahead of 2018-19 series of elections & political populism; PSBS recaps may

be another challenge to fix India’s twin B/S pains.

Today Nifty was helped mostly by Tata Motors, HDFC

Bank, HDFC, Bharti Infratel, ONGC, Indusind Bank, UPL, VEDL, HCL Tech and

M&M by almost 83 points altogether.

Nifty was dragged mostly by Eicher Motors, IOC,

SBI, IBULLS HSG, L&T, Bharti Airtel,. Maruti, ITC, HPCL & Axis Bank by

around 70 points cumulatively.

Overall, today Indian market was helped by mixed

automobiles (mixed Dec sales), financials, techs, metals (upbeat China MFG PMI

data yesterday) & selected private banks (HDFC twins), while it was dragged

by PSBS, FMCG, Media, Pharma, Reality, OMC (concern of higher WTI amid renewed

Iran tensions) & consumption stocks.

SGX-NF

No comments:

Post a Comment